Zero-Trust Architectures for Fintechs: Implementing 5 Key Principles by Q3 2026 to Reduce Breach Risk by 30%

Zero-Trust Architectures for Fintechs: Implementing 5 Key Principles by Q3 2026 to Reduce Breach Risk by 30%

The financial technology (Fintech) sector is a hotbed of innovation, driving unprecedented changes in how we manage, spend, and invest our money. However, with this rapid evolution comes an escalating landscape of cyber threats. Fintech companies, by their very nature, handle vast amounts of sensitive financial data, making them prime targets for sophisticated cyberattacks. Data breaches in this sector can lead to catastrophic financial losses, severe reputational damage, and a complete erosion of customer trust. Traditional perimeter-based security models are proving increasingly insufficient against modern, agile attackers who often bypass these defenses by exploiting internal vulnerabilities or compromised credentials.

This is where Fintech Zero-Trust Security architectures emerge not just as a recommendation, but as an imperative. Zero Trust is a strategic approach to cybersecurity that assumes no user, device, or application should be trusted by default, regardless of whether they are inside or outside the organizational network. Instead, every access request must be explicitly verified. This paradigm shift moves away from the ‘trust but verify’ model to a rigorous ‘never trust, always verify’ philosophy. For Fintechs, adopting Zero Trust isn’t merely about bolstering defenses; it’s about fundamentally rethinking how security is integrated into every layer of their operations.

Our objective in this comprehensive guide is to delve deep into the critical need for Zero-Trust architectures within the Fintech ecosystem. We will outline five key principles that are foundational to its successful implementation. Furthermore, we aim to demonstrate how a diligent adoption of these principles can significantly reduce breach risk—by an ambitious 30%—by the third quarter of 2026. This isn’t just a theoretical goal; it’s a measurable outcome that forward-thinking Fintechs can and should strive for to safeguard their future and their customers’ financial well-being.

The Evolving Threat Landscape for Fintechs

Before diving into the solutions, it’s crucial to understand the challenges. Fintechs operate in a unique environment characterized by rapid digital transformation, extensive use of cloud services, reliance on third-party APIs, and a constant stream of new financial products. This dynamic ecosystem creates numerous attack vectors that traditional security models struggle to cover. Ransomware attacks, phishing campaigns targeting financial credentials, insider threats, and sophisticated nation-state-sponsored cyber espionage are just some of the dangers lurking. The average cost of a data breach continues to rise, and for Fintechs, these costs are often exacerbated by regulatory fines (e.g., GDPR, CCPA) and the irreparable harm to customer confidence.

Moreover, the interconnected nature of the Fintech world means that a vulnerability in one system, or even a third-party vendor, can have a cascading effect across an entire network of financial services. Supply chain attacks, where attackers compromise a less secure vendor to gain access to a larger target, are becoming increasingly prevalent. This complex and hostile environment necessitates a security model that is adaptive, pervasive, and resilient – qualities inherent in a well-implemented Fintech Zero-Trust Security framework.

What is Zero Trust and Why is it Critical for Fintechs?

At its core, Zero Trust rejects the implicit trust traditionally granted to users and devices within a network perimeter. It operates on the principle that threats can originate from anywhere, both inside and outside the network. Therefore, every request for access to resources must be treated as if it originates from an untrusted network. This continuous verification process significantly reduces the attack surface and limits the potential damage should a breach occur.

For Fintechs, this approach offers several compelling advantages:

- Enhanced Data Protection: By segmenting networks and enforcing granular access controls, Zero Trust minimizes the lateral movement of attackers, protecting sensitive financial data more effectively.

- Improved Regulatory Compliance: Many financial regulations (e.g., PCI DSS, SOC 2, ISO 27001) align with Zero Trust principles, making compliance easier to achieve and demonstrate.

- Reduced Attack Surface: Continuous verification and least-privilege access reduce the number of exploitable entry points for attackers.

- Resilience Against Insider Threats: Zero Trust mitigates the risk posed by malicious insiders or compromised legitimate accounts by restricting their access to only what is absolutely necessary for their role.

- Secure Cloud Adoption: As Fintechs increasingly leverage cloud services, Zero Trust provides a consistent security model that extends across hybrid and multi-cloud environments, ensuring data protection regardless of its location.

5 Key Principles of Fintech Zero-Trust Security Implementation

Implementing a robust Fintech Zero-Trust Security architecture requires a strategic, phased approach. Here are five foundational principles that Fintechs must embrace to achieve significant risk reduction by Q3 2026:

1. Verify Explicitly: Never Trust, Always Verify

The cornerstone of Zero Trust is explicit verification for every access attempt. This means abandoning the assumption that once a user or device is inside the network, they are inherently trustworthy. Instead, every request to access a resource must be authenticated and authorized based on all available data points.

- Multi-Factor Authentication (MFA) Everywhere: MFA should be mandated for all users, administrators, and critical systems. This adds a crucial layer of security beyond just passwords. Fintechs should consider adaptive MFA, where the verification method’s strength scales with the risk profile of the access attempt.

- Context-Based Access Decisions: Access decisions should not solely rely on identity. They must incorporate context such as user role, location, device health (e.g., patched, uncompromised), time of day, and the sensitivity of the resource being accessed. A user attempting to access a critical financial ledger from a new, unregistered device in an unusual geographic location should trigger higher scrutiny or block access entirely.

- Continuous Verification: Authentication is not a one-time event. User and device identities, as well as their access privileges, should be continuously re-evaluated throughout a session. If a user’s context changes (e.g., they connect from a public Wi-Fi network), their access might be automatically downgraded or revoked.

- Device Identity and Health: Every device connecting to the network, whether corporate-owned or personal (BYOD), must be identified, authenticated, and continuously monitored for security posture. Devices that don’t meet security baselines (e.g., missing patches, detected malware) should be denied access or quarantined.

For Fintechs, this principle is paramount. The financial industry is a prime target for credential stuffing and phishing attacks. By implementing robust MFA and context-aware access, they can drastically reduce the success rate of such attacks, thereby protecting sensitive customer data and financial transactions. Achieving this by Q3 2026 implies a comprehensive rollout of MFA across all internal and customer-facing applications, alongside the integration of sophisticated identity and access management (IAM) solutions capable of real-time context evaluation.

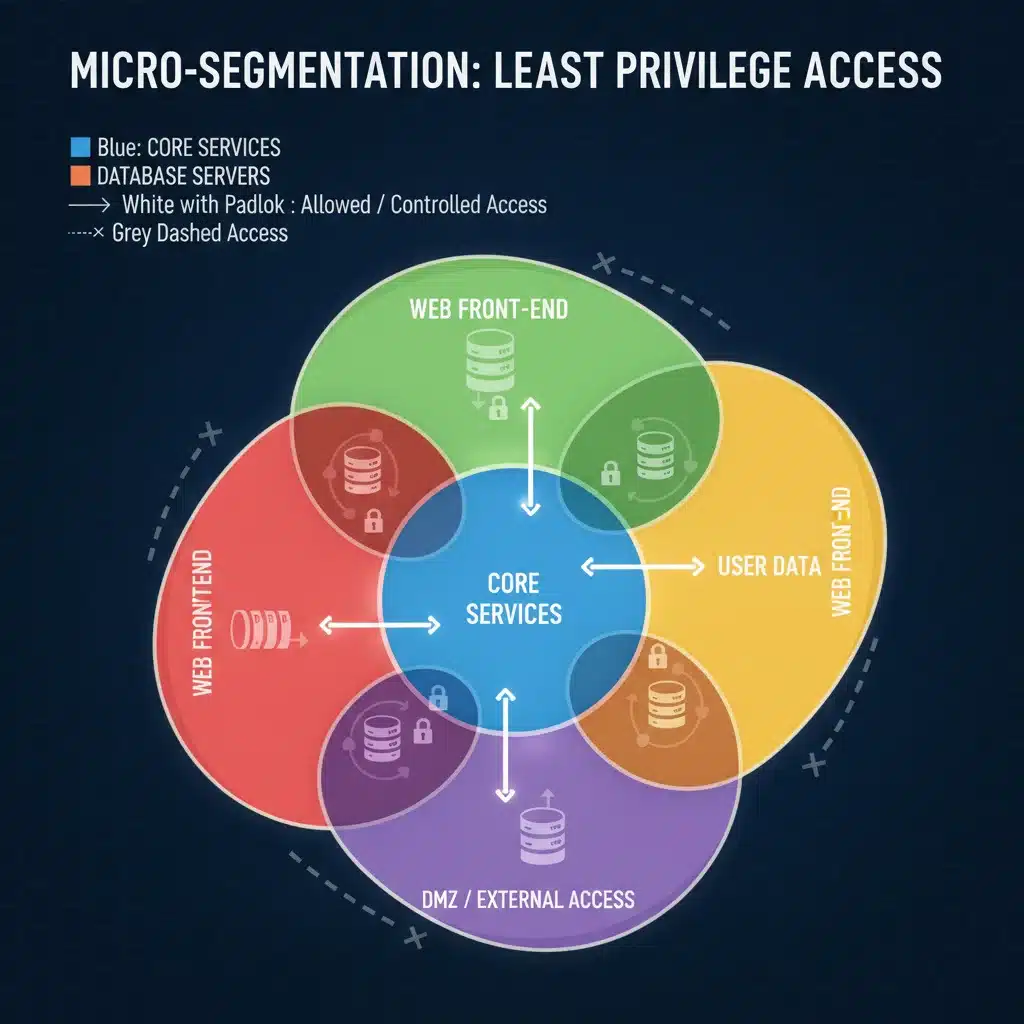

2. Enforce Least Privilege Access: Grant Only What is Needed

The principle of least privilege dictates that users, applications, and devices should only be granted the minimum level of access necessary to perform their legitimate functions, and for the shortest possible duration. This significantly limits the potential damage an attacker can inflict if they manage to compromise an account or system.

- Role-Based Access Control (RBAC) and Attribute-Based Access Control (ABAC): Implement granular RBAC and ABAC policies to define exactly what resources each role or attribute group can access. For instance, a customer service agent might only need read-only access to certain transaction histories, while a financial analyst might require write access to specific reporting tools.

- Just-in-Time (JIT) and Just-Enough Access (JEA): Access to critical systems and sensitive data should be granted on a temporary, as-needed basis. Instead of permanent administrative privileges, users request elevated access for a specific task, and it’s automatically revoked once the task is complete or the time limit expires.

- Micro-segmentation: This involves dividing the network into small, isolated segments, each with its own security controls. If one segment is compromised, the attacker’s ability to move laterally to other segments is severely restricted. For Fintechs, this means isolating payment processing systems from customer databases, or separating development environments from production.

- Regular Access Reviews: Periodically review and audit access privileges to ensure they are still appropriate and necessary. Stale accounts or over-privileged users are common attack vectors.

Implementing least privilege access is a complex undertaking, especially in large Fintech organizations with numerous applications and diverse user roles. However, it’s a non-negotiable component of Fintech Zero-Trust Security. By Q3 2026, Fintechs should aim to have comprehensive micro-segmentation in place for their critical infrastructure and a mature JIT/JEA program for administrative and high-risk accounts.

3. Assume Breach: Prepare for the Inevitable

A core tenet of Zero Trust is to assume that a breach is inevitable, or perhaps has already occurred. This mindset shifts the focus from purely preventive measures to robust detection, response, and containment capabilities. It’s about building resilience into the system, not just erecting walls.

- Continuous Monitoring and Threat Detection: Implement advanced security information and event management (SIEM) and security orchestration, automation, and response (SOAR) solutions. These tools provide real-time visibility into network activity, user behavior, and system logs, enabling rapid detection of anomalies and potential threats. User and Entity Behavior Analytics (UEBA) can be particularly effective in identifying insider threats or compromised accounts.

- Incident Response Plan: Develop and regularly test a comprehensive incident response plan. This plan should detail procedures for identifying, containing, eradicating, recovering from, and learning from security incidents. Regular simulations and tabletop exercises are crucial for ensuring the plan’s effectiveness.

- Data Encryption Everywhere: All sensitive data, both at rest and in transit, should be encrypted using strong, industry-standard encryption protocols. This ensures that even if an attacker gains access to data, it remains unintelligible without the decryption key.

- Automated Remediation: Leverage automation to respond to detected threats swiftly. For example, if a device shows signs of compromise, it can be automatically quarantined, or a user’s session terminated.

For Fintechs, the financial impact and reputational damage of a breach can be devastating. By Q3 2026, a mature Fintech Zero-Trust Security posture means having a fully operational security operations center (SOC) or managed detection and response (MDR) service, coupled with a well-rehearsed incident response strategy that minimizes the dwell time of attackers and the impact of any breach.

4. Log and Monitor All Traffic: Gain Full Visibility

Visibility is paramount in a Zero-Trust environment. Every access request, every data transfer, and every system interaction must be logged, monitored, and analyzed. This provides the necessary intelligence to verify explicitly, enforce least privilege, and assume breach effectively.

- Centralized Logging: Aggregate logs from all endpoints, servers, network devices, applications, and cloud services into a centralized platform. This ensures a holistic view of activity across the entire IT estate.

- Behavioral Analytics: Employ tools that analyze user and system behavior to establish baselines and detect deviations that could indicate malicious activity. For example, an application suddenly accessing an unusual database or a user logging in at an odd hour could be flagged.

- Network Traffic Analysis (NTA): Monitor network traffic for suspicious patterns, unauthorized communications, and data exfiltration attempts. This is especially important for identifying lateral movement within micro-segmented networks.

- Audit Trails and Forensics: Maintain detailed, immutable audit trails for all critical actions. These logs are indispensable for forensic investigations after an incident, helping to understand how a breach occurred and what data was affected.

Without comprehensive logging and monitoring, the other Zero-Trust principles become significantly less effective. Fintechs must invest in robust logging infrastructure and analytical capabilities. By Q3 2026, the goal should be to have near real-time visibility into all critical systems and data flows, enabling proactive threat hunting and rapid anomaly detection to bolster Fintech Zero-Trust Security.

5. Automate and Orchestrate Security Workflows: Efficiency and Scalability

Manual security processes are slow, error-prone, and cannot keep pace with the dynamic nature of modern cyber threats or the scale of Fintech operations. Automation and orchestration are crucial for efficient and scalable Zero-Trust implementation.

- Automated Policy Enforcement: Policies for access control, device compliance, and security configurations should be automated. This ensures consistent application of rules and reduces the potential for human error.

- Security Orchestration, Automation, and Response (SOAR): SOAR platforms integrate various security tools and automate repetitive tasks, such as threat intelligence gathering, incident triage, and response actions. This frees up security analysts to focus on more complex threats.

- Cloud Security Posture Management (CSPM) and Cloud Workload Protection Platforms (CWPP): For Fintechs heavily reliant on cloud infrastructure, automated CSPM and CWPP tools are essential to continuously monitor cloud configurations for misconfigurations and vulnerabilities, ensuring that Zero-Trust principles extend seamlessly into the cloud.

- Identity Governance and Administration (IGA): Automate the lifecycle of identities and their access rights, from provisioning and de-provisioning to access reviews. This ensures that access is granted and revoked efficiently and consistently.

Automation is not just about speed; it’s about consistency and reducing the attack surface by eliminating configuration drift and human error. By Q3 2026, Fintechs should aim to have a significant portion of their security workflows automated, particularly those related to identity and access management, threat detection, and initial incident response. This level of automation is key to achieving a 30% reduction in breach risk by making their Fintech Zero-Trust Security architecture both effective and sustainable.

Roadmap to 30% Breach Risk Reduction by Q3 2026

Achieving a 30% reduction in breach risk within the next two years is an ambitious but attainable goal for Fintechs committed to Zero Trust. Here’s a high-level roadmap:

Phase 1: Assessment and Planning (Now – Q4 2024)

- Current State Assessment: Conduct a thorough audit of existing security posture, identifying critical assets, data flows, and current vulnerabilities.

- Define Scope and Vision: Clearly define the scope of the Zero-Trust initiative, outlining specific objectives and desired outcomes.

- Stakeholder Buy-in: Secure commitment from leadership, IT, and business units.

- Technology Stack Evaluation: Identify necessary tools and platforms for IAM, MFA, micro-segmentation, logging, and automation.

- Pilot Project: Start with a small, contained pilot project to test Zero-Trust principles and gain initial experience.

Phase 2: Initial Implementation and Integration (Q1 2025 – Q2 2026)

- Identity and Access Management (IAM) Overhaul: Implement robust MFA across all critical systems and begin rolling out context-based access policies.

- Micro-segmentation Rollout: Begin segmenting critical networks and applications, starting with the most sensitive data.

- Centralized Logging & Monitoring: Implement SIEM/SOAR platforms and ensure comprehensive logging across the infrastructure.

- Data Encryption: Ensure all sensitive data at rest and in transit is adequately encrypted.

- Automated Workflows: Start automating basic security tasks and policy enforcement.

Phase 3: Optimization and Expansion (Q3 2026 Onwards)

- Continuous Improvement: Regularly review and refine Zero-Trust policies based on threat intelligence and internal audits.

- Expand Coverage: Extend Zero-Trust principles to less critical systems, third-party integrations, and remote workforces.

- Advanced Analytics: Leverage AI/ML for advanced threat detection and behavioral analytics.

- Regular Testing: Conduct frequent penetration testing, red teaming, and incident response drills.

- Compliance Integration: Continuously align Zero-Trust practices with evolving regulatory requirements.

Challenges and Considerations for Fintechs

While the benefits of Fintech Zero-Trust Security are clear, implementing it is not without its challenges:

- Complexity: Large, legacy systems and complex architectures can make micro-segmentation and policy enforcement difficult.

- Cost: Initial investment in new tools, training, and skilled personnel can be substantial.

- User Experience: Overly stringent security measures can sometimes hinder user productivity. A balance must be struck.

- Cultural Shift: It requires a fundamental shift in mindset across the organization, from IT to end-users.

- Third-Party Risk: Extending Zero-Trust to third-party vendors and partners requires careful negotiation and integration.

Fintechs must address these challenges proactively. Phased implementation, starting with critical assets, can help manage complexity. Investing in user-friendly security solutions and comprehensive training can ease the cultural transition. Furthermore, robust vendor risk management frameworks are essential for extending Zero Trust beyond the organizational perimeter.

Conclusion: Securing the Future of Fintech with Zero Trust

The imperative for robust cybersecurity in the Fintech sector has never been greater. As financial services become increasingly digital and interconnected, the traditional ‘castle-and-moat’ security model is no longer viable. Fintech Zero-Trust Security offers a modern, adaptive, and resilient framework that is uniquely suited to address the sophisticated threats facing this industry.

By diligently implementing the five key principles – verify explicitly, enforce least privilege access, assume breach, log and monitor all traffic, and automate and orchestrate security workflows – Fintech companies can build a formidable defense against cyberattacks. The goal of reducing breach risk by 30% by Q3 2026 is ambitious, but entirely achievable with a strategic, committed, and comprehensive adoption of Zero-Trust architectures. This proactive approach will not only protect sensitive financial data and ensure regulatory compliance but also bolster customer trust, safeguarding the future growth and innovation of the entire Fintech ecosystem. The time to embrace Zero Trust is now.