Tokenization Trends: Protecting 95% of US Digital Transactions from Fraud by 2026

Tokenization is set to protect 95% of US digital transactions from fraud by 2026, transforming payment security by replacing sensitive data with unique, non-sensitive tokens, a crucial advancement for digital payments and cybersecurity.

The landscape of digital payments is evolving at an unprecedented pace, and at its core, the push for enhanced security is paramount. By 2026, it is projected that tokenization trends fraud protection will safeguard an astounding 95% of US digital transactions. This isn’t merely an incremental improvement; it represents a fundamental shift in how we approach payment security, moving towards a more resilient and trustworthy digital financial ecosystem.

Understanding tokenization: The foundation of modern payment security

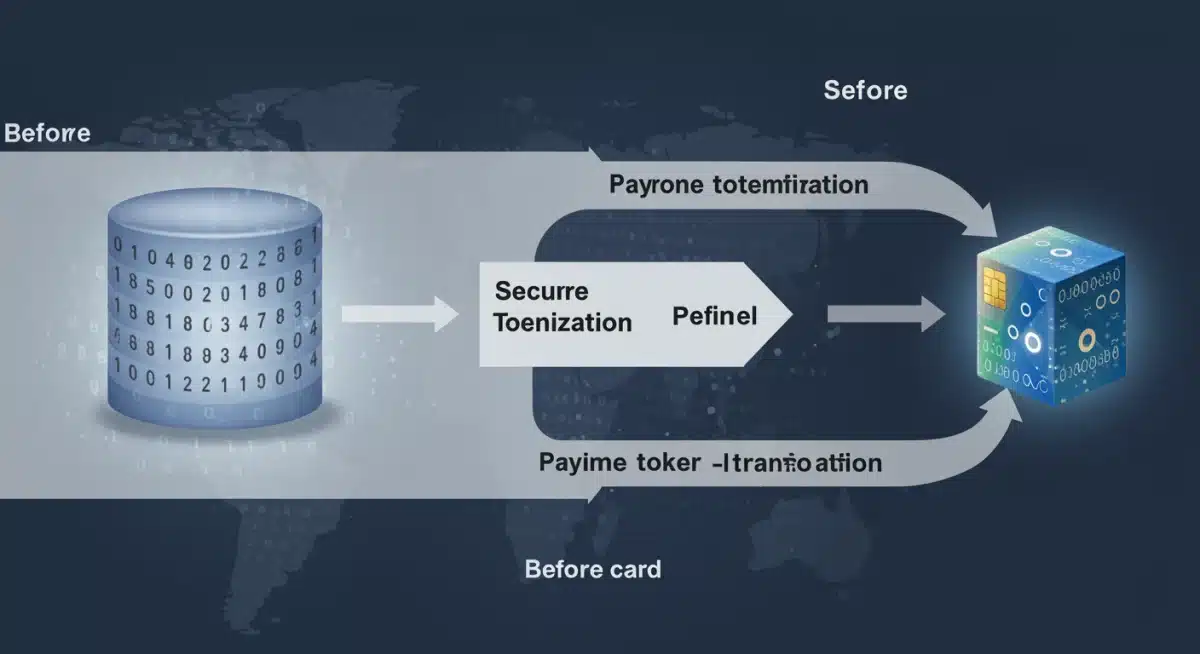

Tokenization is a security technology that replaces sensitive data, such as credit card numbers, with a unique, non-sensitive identifier called a token. This token holds no intrinsic value and cannot be reverse-engineered to reveal the original data, even if intercepted by fraudsters. It’s a critical component in the fight against cybercrime within digital payments.

The concept isn’t new, but its widespread adoption and technological sophistication are reaching new heights. As digital transactions become the norm, the need for robust protection against data breaches and fraud escalates. Tokenization provides a powerful shield, making stolen data useless to malicious actors.

How tokenization works in practice

When a customer initiates a transaction, their sensitive payment information is captured and immediately converted into a token by a secure tokenization platform. This token is then used to process the payment, while the original data is securely stored in a separate, highly protected vault. This process ensures that even if a merchant’s system is compromised, the actual cardholder data remains safe.

- Data replacement: Sensitive card data is swapped for a random, algorithmically generated token.

- Reduced scope: Merchants no longer store raw card data, significantly reducing their PCI DSS compliance burden.

- Enhanced security: Tokens are useless outside the specific transaction or system they are intended for.

- Seamless experience: The tokenization process is invisible to the end-user, maintaining a smooth payment flow.

The beauty of tokenization lies in its simplicity and effectiveness. It addresses the root cause of many data breaches by removing the sensitive information from the transaction stream and merchant’s direct control. This proactive approach is what makes it so vital for the future of digital payments.

The surge in tokenization adoption: Why now?

The rapid acceleration in tokenization adoption isn’t accidental; it’s a response to evolving threats and regulatory pressures. Data breaches continue to be a significant concern for consumers and businesses alike, leading to increased demand for more secure payment methods. Furthermore, regulatory bodies and payment networks are increasingly advocating for tokenization as a best practice.

Merchants, payment processors, and financial institutions are recognizing the tangible benefits of implementing tokenization. Beyond fraud reduction, it offers streamlined compliance processes and enhances customer trust, which are invaluable assets in a competitive market.

Key drivers for widespread tokenization

Several factors contribute to the current momentum behind tokenization. The increasing sophistication of cyberattacks necessitates more advanced defense mechanisms. Traditional encryption, while important, often falls short when data is in transit or at rest within vulnerable systems.

- Rising fraud rates: The sheer volume and complexity of digital payment fraud demand stronger countermeasures.

- Regulatory mandates: Stricter data protection laws push businesses to adopt robust security solutions.

- Consumer demand: Customers expect their financial data to be protected, driving businesses to invest in better security.

- Technological advancements: Improved tokenization platforms make implementation easier and more scalable.

The collective understanding that a single data breach can have catastrophic consequences for a business’s reputation and bottom line has propelled tokenization from a niche solution to a mainstream necessity. This shift is particularly evident in the US market, where digital transactions are a cornerstone of the economy.

Impact on US digital transactions: A safer financial ecosystem

The projected protection of 95% of US digital transactions by 2026 through tokenization is a monumental achievement. This level of security will dramatically reduce financial fraud, instill greater consumer confidence, and foster further innovation in the digital payments space. It signifies a maturation of the digital economy where security is no longer an afterthought but an integral part of the design.

For consumers, this means fewer instances of identity theft and unauthorized transactions, leading to a more secure and stress-free online shopping experience. For businesses, it translates to lower fraud-related losses, reduced operational costs associated with dispute resolution, and a stronger brand reputation built on trust.

Benefits for various stakeholders

The ripple effects of widespread tokenization extend across the entire financial ecosystem. Each stakeholder stands to gain significantly from this enhanced security posture.

Merchants and businesses

Merchants will experience a substantial decrease in chargebacks and fraud-related losses. The burden of PCI DSS compliance is also eased, as they no longer handle sensitive cardholder data directly. This allows them to focus more on their core business operations rather than complex security protocols.

Consumers

Consumers will enjoy greater peace of mind when making online purchases, knowing their financial information is protected. The fear of data breaches and the hassle of replacing compromised cards will be significantly reduced, encouraging more frequent and confident use of digital payment methods.

Financial institutions and payment processors

These entities will benefit from a reduction in fraud investigation costs and improved overall system integrity. Tokenization allows them to process transactions more securely and efficiently, strengthening their position as trusted intermediaries in the digital payment landscape.

Ultimately, a safer financial ecosystem benefits everyone, creating a virtuous cycle where security drives trust, and trust drives growth in digital payments.

Challenges and considerations in widespread tokenization deployment

While the benefits of tokenization are clear, its widespread deployment is not without challenges. Integrating tokenization solutions into existing payment infrastructures can be complex, requiring significant investment in technology and expertise. Compatibility issues between different systems and standards also need to be addressed to ensure seamless operation across the diverse payment landscape.

Another consideration is the ongoing management of tokens. While tokens themselves are non-sensitive, the underlying systems that generate and manage them must be rigorously secured. This requires continuous monitoring, updates, and adherence to best practices in cybersecurity.

Overcoming implementation hurdles

Successful tokenization requires a strategic approach that considers both technological and operational aspects. Collaboration among various stakeholders is crucial to establish common standards and facilitate interoperability.

- Integration complexity: Ensuring tokenization solutions seamlessly integrate with legacy systems.

- Cost of implementation: Initial investments in technology and training can be substantial.

- Standardization: The need for consistent tokenization standards across different payment networks.

- Vendor selection: Choosing reliable tokenization providers with proven security records.

Despite these challenges, the long-term benefits of enhanced security and fraud reduction far outweigh the initial hurdles. As technology evolves, tokenization solutions are becoming more accessible and easier to implement, paving the way for broader adoption.

The role of advanced tokenization in future payment innovation

Tokenization is not a static technology; it’s continuously evolving, paving the way for future innovations in digital payments. Advanced tokenization techniques, such as network tokenization, offer even greater security and flexibility. Network tokens are issued by payment networks (like Visa or Mastercard) and can be used across multiple merchants and devices, further streamlining the payment process while maintaining high security.

This evolution allows for new payment experiences, such as one-click checkouts, subscription services, and in-app purchases, to be delivered with enhanced security. As new payment channels and methods emerge, tokenization will remain a foundational element, adapting to secure these innovations.

Tokenization and emerging payment technologies

The synergy between tokenization and other emerging technologies is particularly exciting. For instance, its integration with biometric authentication can create an even more secure and convenient payment experience.

Biometric authentication

When combined with biometrics (fingerprint, facial recognition), tokenization offers a multi-layered security approach. Biometrics verify the user’s identity, while tokenization protects the payment data, creating an almost impenetrable defense against fraud.

Internet of Things (IoT) payments

As IoT devices become payment-enabled, tokenization will be crucial for securing transactions initiated from smart appliances, wearables, and connected cars. Each device can be assigned a unique token, ensuring that even if a device is compromised, the broader payment ecosystem remains secure.

Central bank digital currencies (CBDCs)

While still in their nascent stages, CBDCs could also leverage tokenization for enhanced privacy and security, ensuring that digital currency transactions are both secure and traceable without revealing personal financial details.

The future of digital payments is intrinsically linked to the advancements in tokenization, promising a landscape that is not only more secure but also more innovative and user-friendly.

Beyond 2026: Sustaining tokenization’s dominance in fraud prevention

Achieving 95% protection of US digital transactions by 2026 is a significant milestone, but sustaining tokenization’s dominance in fraud prevention requires continuous effort and adaptation. Fraudsters are constantly evolving their tactics, necessitating ongoing innovation in security measures. This means that tokenization solutions must be dynamic, capable of adapting to new threats and technological shifts.

Collaboration between industry players, regulatory bodies, and cybersecurity experts will be essential to maintain a proactive stance against fraud. Sharing threat intelligence, developing common standards, and investing in research and development will ensure that tokenization remains at the forefront of payment security.

Future considerations for tokenization

To ensure tokenization continues to be effective, several key areas will require focus beyond 2026. These include:

- Quantum computing threats: Developing quantum-resistant tokenization algorithms to future-proof systems.

- AI and machine learning: Integrating AI for real-time fraud detection and adaptive tokenization strategies.

- Global interoperability: Expanding tokenization standards to ensure seamless cross-border transactions.

- User education: Continuing to educate consumers and businesses on the benefits and proper use of tokenized payments.

The journey towards a fully secure digital payment ecosystem is ongoing, but tokenization provides a robust and adaptable framework. Its continued evolution will be critical in safeguarding the integrity of digital transactions well into the future, ensuring that the US remains a leader in secure digital commerce.

| Key Aspect | Description |

|---|---|

| Fraud Reduction Goal | Protecting 95% of US digital transactions from fraud by 2026. |

| Core Mechanism | Replaces sensitive data with unique, non-sensitive tokens. |

| Key Benefits | Enhanced security, reduced compliance burden, increased consumer trust. |

| Future Outlook | Adaptation to new threats, integration with AI, quantum-resistant algorithms. |

Frequently asked questions about tokenization and fraud prevention

Tokenization is a security method that replaces sensitive payment data, like credit card numbers, with a randomly generated, non-sensitive identifier called a token. This token is used for transactions, while the original data is securely stored, making intercepted tokens useless to fraudsters.

By replacing actual card data with tokens, tokenization ensures that even if a merchant’s system is breached, the stolen information is meaningless to criminals. This significantly reduces the risk of data compromise and subsequent fraudulent transactions, acting as a powerful deterrent.

Achieving 95% fraud protection by 2026 signifies a major leap in securing US digital transactions. This goal enhances consumer trust, reduces financial losses for businesses, and streamlines compliance, paving the way for a more robust and reliable digital economy.

Consumers benefit from increased security and peace of mind. Their sensitive payment information is less exposed, reducing the risk of identity theft and unauthorized charges. This leads to a more confident and hassle-free experience when engaging in online or digital transactions.

Challenges include integrating tokenization solutions with existing payment infrastructures, the initial cost of implementation, and establishing universal standards for interoperability. Continuous management and adaptation to evolving cyber threats are also crucial for long-term effectiveness.

Conclusion

The journey towards protecting 95% of US digital transactions from fraud by 2026 through advanced tokenization is a testament to the industry’s commitment to security and innovation. This transformative trend is not just about preventing financial losses; it’s about building a foundation of trust that underpins the entire digital economy. As tokenization continues to evolve, integrating with new technologies and adapting to emerging threats, it will remain an indispensable tool in safeguarding our digital financial future. The proactive adoption of these robust security measures ensures that the US digital payments landscape will be more resilient, secure, and ready for the challenges and opportunities that lie ahead.