US Digital Payments 2026: 5 Key Trends Reshaping Consumer Spending Habits

US Digital Payments 2026: 5 Key Trends Reshaping Consumer Spending Habits

The landscape of US digital payments is undergoing a profound transformation, driven by technological advancements, evolving consumer expectations, and a competitive fintech ecosystem. As we look ahead to 2026, several pivotal trends are set to redefine how Americans spend, save, and interact with their money. This comprehensive exploration delves into five key areas that will fundamentally reshape consumer spending habits and offer both opportunities and challenges for businesses and financial institutions alike. Understanding these shifts is not merely an academic exercise; it’s a strategic imperative for anyone operating within or impacted by the financial sector.

The rapid acceleration of digital adoption, spurred by recent global events, has permanently altered consumer behavior. Convenience, speed, and security are no longer mere preferences but baseline expectations. As a result, the US digital payments market is experiencing an unprecedented period of innovation, with new solutions emerging that promise to make transactions more seamless, integrated, and personalized than ever before. From the ubiquity of mobile wallets to the promise of real-time transactions, and from the security of biometrics to the integration of financial services into everyday apps, the future of payments is dynamic and exciting.

This article will dissect each of these five critical trends, providing a detailed analysis of their impact on consumer spending habits, the technological underpinnings driving their adoption, and the strategic implications for businesses. We will also consider the regulatory environment and the challenges that must be addressed to ensure a secure and equitable digital payment future. By 2026, the way we pay will look dramatically different, and being prepared for these changes is key to thriving in the evolving digital economy.

1. The Ascendancy of Mobile Wallets: More Than Just a Payment Method

Mobile wallets have already become a familiar sight, but their influence on US digital payments is set to expand exponentially by 2026. Beyond merely storing credit and debit card information, modern mobile wallets are evolving into comprehensive financial hubs, integrating loyalty programs, public transport passes, digital IDs, and even investment features. This consolidation of services within a single, easily accessible application significantly enhances convenience for consumers, making them increasingly reliant on their smartphones for virtually all financial interactions.

The growth of mobile wallets is driven by several factors. Firstly, the widespread ownership of smartphones provides a fertile ground for adoption. Secondly, the seamless user experience, often involving just a tap or a scan, reduces friction at the point of sale, whether online or in-store. Thirdly, enhanced security features, such as tokenization and biometric authentication, offer consumers greater peace of mind compared to traditional card-based transactions. Companies like Apple Pay, Google Pay, and Samsung Pay are leading this charge, continually adding new functionalities and expanding their acceptance networks.

Impact on Consumer Spending Habits

- Increased Digital-First Mentality: Consumers will increasingly prefer their mobile devices for all transactions, reducing reliance on physical cards and cash.

- Enhanced Loyalty and Personalization: Integrated loyalty programs within mobile wallets will drive repeat business and allow for highly personalized offers based on spending patterns.

- Budgeting and Financial Management: Advanced mobile wallets may offer built-in budgeting tools, helping consumers track spending and make more informed financial decisions directly from their payment app.

- Cross-Channel Consistency: A consistent payment experience across online, in-app, and in-store channels will become the norm, blurring the lines between different retail environments.

For businesses, embracing mobile wallets means more than just accepting them at checkout. It involves integrating these platforms into broader customer engagement strategies, leveraging the data they provide for insights, and exploring opportunities for in-app purchasing and personalized marketing. The battle for mobile wallet dominance will intensify, with traditional financial institutions, tech giants, and innovative fintech startups all vying for a share of this rapidly expanding market in US digital payments.

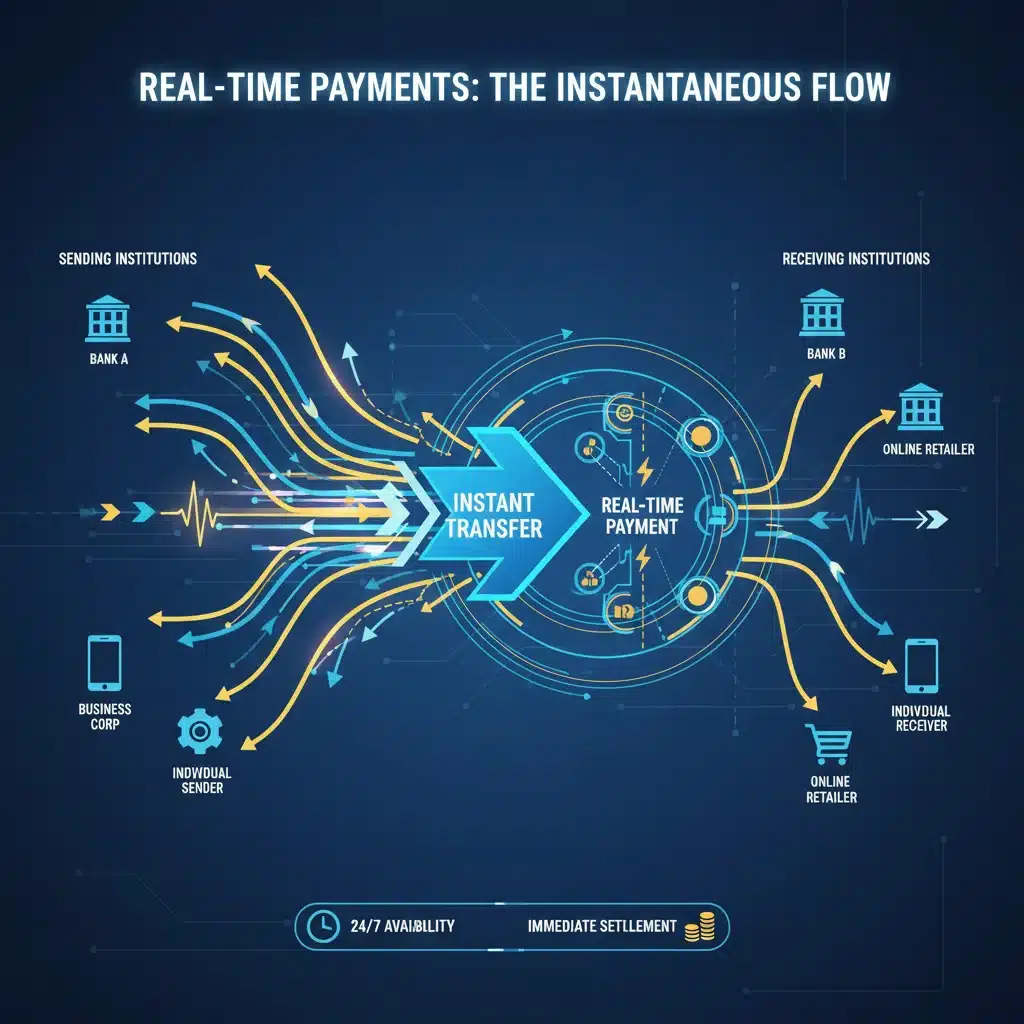

2. The Rise of Real-Time Payments: Speed and Efficiency Redefined

Real-time payments (RTP) are poised to revolutionize the speed and efficiency of financial transactions across the US. Unlike traditional payment systems that can take days to clear, RTP networks enable instant settlement and availability of funds, 24/7, 365 days a year. The Federal Reserve’s introduction of FedNow in 2023, alongside The Clearing House’s RTP network, marks a significant milestone in accelerating the adoption of instant payments. This development is not just about faster money movement; it’s about unlocking new economic opportunities and improving cash flow for both consumers and businesses.

For consumers, RTP means immediate access to wages, instant bill payments, and faster peer-to-peer transfers. Imagine receiving your paycheck and being able to pay an urgent bill or transfer money to a family member within seconds, regardless of the time or day. This eliminates the anxiety and inconvenience associated with pending transactions and provides greater control over personal finances. For businesses, the benefits are even more profound, including improved liquidity management, faster invoice payments from customers, and the ability to pay suppliers and employees instantly.

Impact on Consumer Spending Habits

- Improved Cash Flow Management: Consumers will have better control over their finances due to immediate access to funds, potentially reducing reliance on short-term credit.

- Instant Bill Payments: The ability to pay bills instantly can help consumers avoid late fees and manage unexpected expenses more effectively.

- Enhanced P2P Transfers: Peer-to-peer payments will become truly instant, making splitting bills or sending money to friends and family even more seamless.

- New Payment Use Cases: RTP could facilitate new payment models, such as instant refunds, immediate insurance payouts, and on-demand wage access, further integrating financial services into daily life.

The widespread adoption of real-time payments will necessitate significant infrastructure upgrades for financial institutions and businesses. However, the competitive advantage offered by instant transactions, particularly in areas like e-commerce and gig economy payments, will drive rapid uptake. By 2026, real-time payments will be a foundational element of the US digital payments infrastructure, fundamentally altering expectations around transaction speed and efficiency.

3. Biometric Authentication: The Future of Secure Payments

Security remains a paramount concern in the digital age, and biometric authentication is emerging as a leading solution to combat fraud and enhance the user experience in US digital payments. Technologies like fingerprint scanning, facial recognition, and iris scanning are moving beyond unlocking smartphones to securely authorizing transactions. These methods offer a significant leap in security over traditional passwords and PINs, which can be forgotten, stolen, or compromised.

The convenience factor is also a major driver of biometric adoption. Instead of typing in lengthy passwords or remembering multiple PINs, users can complete transactions with a simple touch or glance. This frictionless experience not only speeds up the checkout process but also reduces abandonment rates for online purchases. As biometric technology becomes more sophisticated and affordable, its integration into payment systems, both online and in-store, will become increasingly common.

Impact on Consumer Spending Habits

- Enhanced Security Confidence: Consumers will feel more secure making digital payments, leading to increased trust and usage of online and mobile channels.

- Faster and More Convenient Transactions: The elimination of passwords and PINs will streamline the payment process, making transactions quicker and less cumbersome.

- Reduced Fraud: Biometrics significantly reduce the risk of unauthorized transactions, protecting consumers from financial losses and identity theft.

- Personalized Payment Experiences: Biometric data could also enable more personalized services, although careful consideration of privacy implications will be essential.

While the benefits are clear, challenges remain, particularly around data privacy and the potential for biometric data breaches. Robust encryption and secure storage of biometric templates will be crucial for maintaining consumer trust. Nevertheless, by 2026, biometric authentication will be an integral part of the US digital payments ecosystem, setting a new standard for secure and convenient transactions.

4. Embedded Finance: Payments as a Seamless Part of the Experience

Embedded finance represents a paradigm shift where financial services, including payments, are seamlessly integrated into non-financial platforms and applications. This trend moves beyond simply offering a payment option to making payments an invisible, inherent part of a broader customer journey. Think of ordering food directly within a social media app or paying for a ride-share service without ever opening a separate banking app. The goal is to reduce friction and create a more integrated, intuitive user experience.

This trend is powered by Application Programming Interfaces (APIs) that allow different platforms to communicate and share functionalities. Companies are increasingly recognizing that by embedding financial services directly into their core offerings, they can enhance customer loyalty, create new revenue streams, and gather valuable data insights. This could involve everything from lending and insurance to banking and, crucially, payments, all delivered within the context of a consumer’s existing digital interactions.

Impact on Consumer Spending Habits

- Frictionless Transactions: Payments become an almost invisible part of the user experience, leading to more impulsive and convenient spending.

- Integrated Services: Consumers will access financial services directly within apps they already use for shopping, entertainment, or communication, blurring the lines between different types of platforms.

- Personalized Offers: Platforms can leverage embedded payment data to offer highly relevant products and services at the point of need, potentially influencing purchasing decisions.

- Increased Digital Engagement: The convenience of embedded finance will encourage greater reliance on digital platforms for a wider range of activities.

For businesses, embedded finance offers a powerful way to deepen customer relationships and expand their market reach. Fintech companies, tech giants, and traditional financial institutions are all exploring opportunities in this space, often through partnerships. The competitive landscape for US digital payments will increasingly be defined by who can offer the most seamless and integrated financial experiences, moving payments from a standalone action to an intrinsic part of everyday life.

5. The Growing Influence of Cryptocurrency and Blockchain in Payments

While still nascent in widespread adoption for everyday transactions, cryptocurrency and blockchain technology are poised to exert a growing influence on US digital payments by 2026. Beyond speculative investment, the underlying technology of blockchain offers unique advantages for payments, including enhanced security, transparency, and the potential for lower transaction fees, especially for cross-border payments.

Stablecoins, cryptocurrencies pegged to a stable asset like the US dollar, are emerging as a more viable option for everyday transactions due to their reduced volatility. Major payment processors and financial institutions are already experimenting with or integrating crypto payment options, reflecting a growing acceptance and demand. Furthermore, the concept of Central Bank Digital Currencies (CBDCs) is being actively explored by governments worldwide, including the US, which could fundamentally reshape the digital payment infrastructure.

Impact on Consumer Spending Habits

- Alternative Payment Options: A subset of consumers will increasingly use cryptocurrencies for purchases, especially from merchants who accept them.

- Faster Cross-Border Payments: Blockchain-based payments can significantly reduce the time and cost of international transfers, benefiting consumers with global connections.

- Enhanced Transparency and Security: The immutable nature of blockchain transactions can offer greater transparency and security for certain types of payments.

- Potential for Financial Inclusion: Cryptocurrencies could offer new financial services to unbanked or underbanked populations, though regulatory hurdles remain.

The journey for cryptocurrency to achieve mainstream payment status is still long, facing challenges related to scalability, regulatory clarity, and user education. However, the underlying technological innovations are undeniable. By 2026, while perhaps not replacing traditional methods, crypto and blockchain will carve out a more significant niche in the US digital payments landscape, particularly for specific use cases and a growing segment of tech-savvy consumers.

Challenges and Opportunities in the Evolving Digital Payment Landscape

The rapid evolution of US digital payments presents both significant opportunities and considerable challenges. For consumers, the promise is greater convenience, speed, and security. For businesses, it’s about improved efficiency, new revenue streams, and deeper customer engagement. However, navigating this complex landscape requires careful consideration of several key factors.

Key Challenges

- Security and Fraud Prevention: As digital transactions become more prevalent, so too do the sophisticated methods of cybercriminals. Protecting consumer data and funds against fraud remains a top priority.

- Regulatory Complexity: The pace of technological innovation often outstrips regulatory frameworks. Striking a balance between fostering innovation and ensuring consumer protection and financial stability is crucial.

- Interoperability: The proliferation of different payment systems, mobile wallets, and platforms can lead to fragmentation. Ensuring seamless interoperability across various solutions is essential for a truly frictionless experience.

- Digital Divide: While digital payments offer immense benefits, there’s a risk of exacerbating the digital divide, leaving behind those without access to technology or digital literacy.

- Data Privacy: With more data being collected through digital transactions, concerns about how this data is stored, used, and protected will intensify, requiring robust privacy policies and transparent practices.

Strategic Opportunities

- Enhanced Customer Experience: Businesses that successfully integrate these new payment technologies can offer superior customer experiences, leading to increased loyalty and satisfaction.

- New Business Models: The trends discussed open doors for entirely new business models, particularly in areas like embedded finance and real-time payment services.

- Operational Efficiency: Adopting real-time payments and automated digital processes can significantly reduce operational costs and improve cash flow management for businesses.

- Global Expansion: Digital payment solutions, especially those leveraging blockchain, can simplify cross-border transactions, enabling businesses to expand their reach more easily.

- Personalized Services: The data generated from digital payments, when used ethically and responsibly, can enable highly personalized financial products and services tailored to individual consumer needs.

Addressing these challenges proactively and capitalizing on the opportunities will be critical for success in the US digital payments market of 2026. Collaboration between fintech innovators, traditional financial institutions, regulators, and consumers will be essential to build a robust, secure, and inclusive digital payment ecosystem.

Conclusion: Navigating the Future of US Digital Payments

The trajectory of US digital payments towards 2026 is one of relentless innovation and profound change. The five trends discussed – the ascendancy of mobile wallets, the rise of real-time payments, the adoption of biometric authentication, the integration of embedded finance, and the growing influence of cryptocurrency – are not isolated phenomena but interconnected forces shaping a new financial paradigm. Consumer spending habits are increasingly digital-first, demanding speed, convenience, and security above all else.

Businesses and financial institutions that embrace these trends and strategically adapt their offerings will be best positioned to thrive. This involves not just adopting new technologies but rethinking customer journeys, prioritizing data security and privacy, and fostering an environment of continuous innovation. The transformation of US digital payments is more than just a technological upgrade; it’s a fundamental shift in how value is exchanged, how financial relationships are built, and how economic activity is conducted.

By understanding these key trends, stakeholders can anticipate future challenges, seize emerging opportunities, and contribute to building a more efficient, secure, and inclusive digital payment ecosystem for all Americans. The future of payments is here, and it’s digital, dynamic, and rapidly evolving.