Zero-Trust Architectures for US Fintechs: Best ROI in 2025

Understanding which zero-trust architecture delivers the best return on investment for US fintechs in 2025 is crucial for robust cybersecurity and sustainable growth. This analysis delves into various models, assessing their efficacy and financial implications.

As the digital landscape evolves, US fintechs face escalating cyber threats, making robust security not just a necessity but a strategic imperative. The question of zero-trust fintech ROI for 2025 security budgets is paramount, guiding decisions on which architectural model best fortifies defenses while optimizing financial returns.

Understanding Zero-Trust: Beyond the Perimeter

Zero-trust security represents a fundamental shift from traditional perimeter-based models, operating on the principle of “never trust, always verify.” This approach assumes that threats can originate from inside or outside the network, requiring continuous authentication and authorization for all users and devices attempting to access resources.

For US fintechs, this paradigm is particularly relevant given the sensitive nature of financial data and the stringent regulatory requirements. Implementing a zero-trust framework helps mitigate risks associated with insider threats, compromised credentials, and sophisticated external attacks that often bypass traditional defenses.

Core Principles of Zero Trust

The foundation of any effective zero-trust architecture rests on several immutable principles that guide its design and implementation. These principles ensure that security is enforced at every access point and for every transaction, regardless of location or device.

- Verify explicitly: Authenticate and authorize every access request based on all available data points, including user identity, location, device health, and service/data classification.

- Least privilege access: Grant users and devices only the minimum access rights necessary to perform their tasks, dynamically adjusting permissions as context changes.

- Assume breach: Design systems and processes with the assumption that a breach is inevitable, implementing micro-segmentation and robust logging to contain and detect threats quickly.

By adhering to these principles, fintechs can establish a more resilient security posture, reducing their attack surface and enhancing their ability to detect and respond to security incidents effectively. This proactive stance is crucial for maintaining customer trust and regulatory compliance in a dynamic threat environment.

In essence, zero trust isn’t a single product but a strategic approach that demands rethinking how access is granted and managed across the entire digital ecosystem. Its comprehensive nature makes it an attractive, albeit complex, solution for the unique security challenges faced by the financial sector.

Traditional Zero-Trust vs. Adaptive Zero-Trust

When considering zero-trust architectures, US fintechs often encounter two primary models: traditional (or foundational) zero trust and adaptive zero trust. Each offers distinct advantages and challenges, impacting the potential ROI for security budgets.

Traditional zero trust focuses on strict, policy-driven access controls, meticulously defining who can access what, under what conditions. This model emphasizes granular segmentation and continuous verification. Adaptive zero trust, however, takes this a step further by incorporating machine learning and artificial intelligence to dynamically assess risk and adjust access policies in real-time, based on behavioral analytics and evolving threat intelligence.

Evaluating Traditional Zero-Trust

Traditional zero trust provides a strong baseline for security, enforcing strict rules and micro-segmentation. Its predictable nature makes it easier to implement in highly regulated environments where policy enforcement is critical. However, it can be rigid, potentially leading to operational friction if policies are not meticulously managed and updated.

- Pros: Clear policy enforcement, strong initial security posture, well-defined control points.

- Cons: Potential for operational overhead, less flexible in dynamic environments, requires significant manual policy management.

- ROI Factor: Lower initial investment in advanced AI/ML capabilities, but higher ongoing operational costs for policy management and updates.

The Rise of Adaptive Zero-Trust

Adaptive zero trust offers enhanced agility and responsiveness, leveraging AI and ML to detect anomalous behavior and automatically adjust access. This dynamic capability is particularly beneficial for fintechs with rapidly changing user bases, diverse device ecosystems, and evolving application landscapes. It can significantly reduce the burden of manual policy management and offer superior threat detection capabilities.

- Pros: Dynamic risk assessment, real-time policy adjustments, improved threat detection, reduced manual effort.

- Cons: Higher initial investment in AI/ML infrastructure, requires specialized expertise for deployment and tuning, potential for false positives if not properly configured.

- ROI Factor: Higher initial investment, but potentially lower long-term operational costs and significantly improved security outcomes, leading to a stronger zero-trust fintech ROI.

Ultimately, the choice between traditional and adaptive zero trust depends on a fintech’s specific needs, existing infrastructure, and risk appetite. While traditional models offer a solid foundation, adaptive zero trust presents a more sophisticated and future-proof solution for the complex challenges of 2025 and beyond.

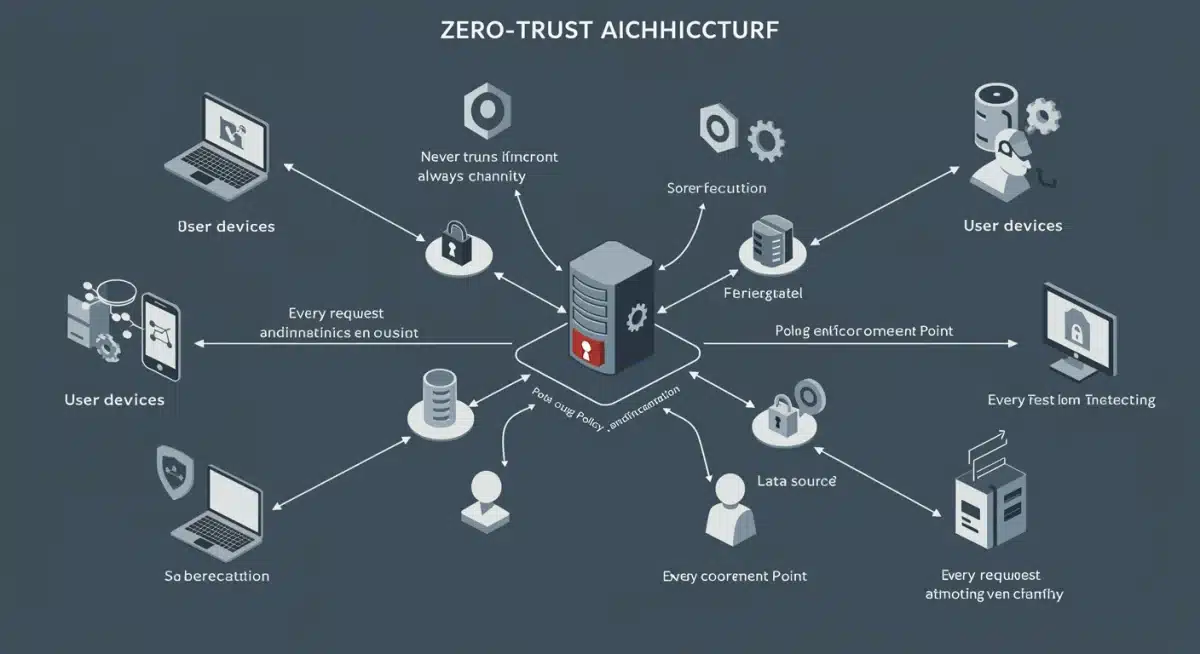

Key Components of a Zero-Trust Architecture for Fintechs

Implementing an effective zero-trust architecture in a fintech environment requires careful consideration of several interconnected components. These elements work in concert to enforce the core principles of never trust, always verify, ensuring comprehensive protection for sensitive financial data and transactions.

A well-designed architecture will integrate identity and access management, device security, micro-segmentation, and continuous monitoring to create a unified and resilient defense. Each component plays a vital role in establishing trust boundaries and enforcing policies across the entire IT ecosystem.

Identity and Access Management (IAM)

At the heart of zero trust lies robust IAM. For fintechs, this means ensuring that every user, whether an employee, partner, or customer, is explicitly identified and authenticated before gaining access to any resource. Multi-factor authentication (MFA) and adaptive authentication are critical here.

- Strong Authentication: Implementing MFA across all access points.

- Single Sign-On (SSO): Streamlining user experience while maintaining security.

- Privileged Access Management (PAM): Securing accounts with elevated permissions.

Effective IAM reduces the risk of credential theft and unauthorized access, which are common vectors for cyberattacks in the financial industry.

Device Security and Endpoint Protection

Devices, from corporate laptops to personal mobile phones used for work, represent potential entry points for attackers. A zero-trust model mandates continuous assessment of device health and compliance before granting access. This includes checking for malware, unpatched vulnerabilities, and adherence to security policies.

Endpoint Detection and Response (EDR) solutions are crucial for monitoring and responding to threats on all connected devices, ensuring that compromised endpoints cannot serve as conduits for wider network breaches. This continuous validation is a cornerstone of maintaining trust.

Network Micro-segmentation

Micro-segmentation involves dividing the network into small, isolated zones, each with its own security controls. This limits the lateral movement of attackers within the network, containing breaches to a small segment rather than allowing them to spread across the entire infrastructure. For fintechs handling diverse types of sensitive data, micro-segmentation is indispensable.

By preventing unauthorized access between segments, even if one segment is compromised, the impact on other critical systems is minimized. This significantly reduces the potential damage and improves recovery times, directly contributing to a better zero-trust fintech ROI.

Continuous Monitoring and Analytics

Zero trust is not a set-it-and-forget-it solution. It requires continuous monitoring of all network activity, user behavior, and system logs to detect anomalies and potential threats. Security Information and Event Management (SIEM) and Security Orchestration, Automation, and Response (SOAR) platforms are essential for correlating data and automating responses.

These tools provide real-time visibility into the security posture, enabling fintechs to identify and remediate threats proactively. The ability to quickly detect and respond to incidents is a critical factor in minimizing financial losses and reputational damage.

Integrating these components effectively creates a robust, adaptive security framework that protects against a wide array of cyber threats. For US fintechs, this integrated approach is key to achieving both strong security and a favorable ROI on their 2025 security investments.

Calculating ROI for Zero-Trust Investments in Fintech

Determining the return on investment (ROI) for cybersecurity initiatives, especially something as comprehensive as zero trust, can be challenging but is essential for US fintechs to justify budget allocations. The ROI for zero trust isn’t just about direct cost savings; it encompasses risk reduction, compliance benefits, and enhanced operational efficiency.

Fintechs must move beyond simply calculating the cost of implementation and consider the broader financial and strategic impacts. This involves assessing both tangible and intangible benefits that accrue over time from a strengthened security posture.

Quantifiable Benefits

Direct cost savings often come from reduced incident response costs, fewer data breaches, and lower compliance fines. A robust zero-trust model can significantly decrease the likelihood and severity of security incidents, leading to substantial savings.

- Reduced Breach Costs: A single data breach can cost millions, including legal fees, regulatory fines, and reputational damage. Zero trust minimizes this risk.

- Operational Efficiency: Automated policy enforcement and streamlined access management can reduce the burden on IT security teams, freeing up resources for other strategic initiatives.

- Insurance Premium Reductions: Demonstrating a strong security posture through zero trust can lead to lower cybersecurity insurance premiums.

Intangible Benefits and Risk Mitigation

Beyond direct financial benefits, zero trust offers significant intangible advantages that contribute to long-term business sustainability. These include improved customer trust, enhanced brand reputation, and better competitive positioning.

- Enhanced Customer Trust: In the financial sector, trust is paramount. Strong security reassures customers that their data is safe, fostering loyalty.

- Improved Brand Reputation: Avoiding public security incidents protects a fintech’s brand and market standing, which can be invaluable.

- Competitive Advantage: A superior security posture can differentiate a fintech in a crowded market, attracting more security-conscious clients.

Furthermore, compliance with regulations like GDPR, CCPA, and upcoming financial industry-specific mandates becomes more manageable with a zero-trust framework. Avoiding non-compliance penalties and maintaining a clean regulatory record are critical for fintechs operating in the US.

To accurately calculate the zero-trust fintech ROI for 2025, organizations should conduct a thorough risk assessment, quantify potential losses from various cyber scenarios, and then assess how zero trust mitigates those risks. This holistic view provides a clearer picture of the investment’s true value, extending beyond immediate financial outlays to encompass long-term strategic gains.

Challenges and Considerations for US Fintechs

While the benefits of zero trust are compelling, US fintechs face several unique challenges and considerations when implementing these architectures. Navigating these complexities is crucial for a successful deployment and for maximizing the ROI.

The highly regulated nature of the financial industry, coupled with the rapid pace of technological change and the need for seamless user experiences, adds layers of difficulty. Addressing these challenges proactively can prevent costly missteps.

Regulatory Compliance and Data Sovereignty

Fintechs operate under a labyrinth of regulations, including GLBA, PCI DSS, and state-specific data privacy laws. Zero trust must be designed to not only meet but exceed these compliance requirements, ensuring data protection and privacy across all operations. Data sovereignty concerns, particularly with cloud-based solutions, also demand careful attention to where data is stored and processed.

Ensuring that all components of the zero-trust architecture align with these diverse regulatory frameworks requires a deep understanding of legal obligations and careful planning during the design phase. Non-compliance can lead to severe penalties and reputational damage.

Integration with Legacy Systems

Many US fintechs, especially those with a history, rely on legacy systems that may not be inherently compatible with modern zero-trust principles. Integrating new security architectures with older infrastructure can be complex, time-consuming, and expensive. It often requires phased implementation and careful interoperability planning.

Addressing this involves strategic API development, middleware solutions, and potentially gradual migration strategies. The goal is to extend zero-trust principles to legacy environments without disrupting critical financial operations.

User Experience vs. Security

Fintech users expect seamless, intuitive experiences. Overly stringent security measures, if not carefully implemented, can introduce friction and negatively impact user adoption and satisfaction. Balancing robust security with a fluid user experience is a delicate act.

This challenge can be mitigated through intelligent design, such as context-aware authentication, single sign-on (SSO), and user-friendly MFA solutions. The key is to make security invisible where possible, only surfacing controls when genuinely necessary based on risk assessment.

Overcoming these challenges requires a strategic, phased approach, strong leadership commitment, and collaboration between security, IT, and business units. By addressing these considerations head-on, US fintechs can build a more effective zero-trust architecture that delivers tangible value and a strong zero-trust fintech ROI.

Future Trends and Best Practices for 2025

As 2025 approaches, the zero-trust landscape for US fintechs continues to evolve, driven by emerging technologies, escalating cyber threats, and changing regulatory demands. Staying ahead of these trends and adopting best practices will be critical for maintaining a competitive edge and robust security posture.

The emphasis will increasingly shift towards more intelligent, automated, and integrated security solutions that can adapt to rapid changes in the threat landscape and business environment.

AI and Machine Learning in Zero Trust

The integration of AI and machine learning will become even more pervasive in zero-trust architectures. These technologies will power advanced behavioral analytics, predictive threat intelligence, and automated policy adjustments, moving beyond traditional rule-based systems. This enables real-time risk assessment and proactive defense against novel threats.

- Predictive Threat Intelligence: AI will analyze vast datasets to anticipate and neutralize threats before they materialize.

- Automated Policy Orchestration: ML-driven systems will dynamically adjust access policies based on context and risk, reducing manual overhead.

Continuous Adaptive Risk and Trust Assessment (CARTA)

CARTA, a Gartner concept, will gain further traction. It emphasizes continuous, adaptive risk and trust assessment, where security decisions are not static but evolve with every interaction. This dynamic approach aligns perfectly with the adaptive zero-trust model, providing ongoing evaluation of trust levels.

For fintechs, CARTA means moving towards an even more granular and context-aware security model, where every access request is evaluated against a constantly updated risk profile, ensuring agile and resilient protection.

Cloud-Native Zero Trust

With the increasing adoption of cloud services, zero-trust architectures will become intrinsically cloud-native. This involves designing security directly into cloud environments, leveraging cloud provider security features, and extending zero-trust principles to microservices, containers, and serverless functions. This ensures consistent security across hybrid and multi-cloud environments.

Best practices for 2025 will include a strong focus on automation, integration, and continuous improvement. Fintechs should prioritize solutions that offer scalability, flexibility, and a high degree of interoperability with existing and future technologies. Regular security audits, employee training, and staying informed about the latest threat intelligence will also remain foundational elements of a strong security strategy.

By embracing these trends and best practices, US fintechs can ensure their zero-trust investments deliver optimal zero-trust fintech ROI, providing superior protection and supporting long-term business growth.

Choosing the Right Zero-Trust Model for Your Fintech

Selecting the most suitable zero-trust model for a US fintech is a critical strategic decision that directly impacts security posture, operational efficiency, and ultimately, ROI. There’s no one-size-fits-all solution; the ideal model depends on various factors specific to each organization.

Fintechs must conduct a thorough assessment of their current security landscape, business objectives, regulatory obligations, and technological capabilities before committing to a particular architecture. This comprehensive evaluation ensures that the chosen model aligns with the company’s unique needs.

Factors to Consider

Several key factors should guide the decision-making process. These include the size and complexity of the organization, the nature of the data handled, the existing IT infrastructure, and the available budget and resources.

- Organizational Size and Complexity: Smaller fintechs might benefit from simpler, more straightforward zero-trust implementations, while larger, more complex organizations may require advanced adaptive models.

- Data Sensitivity: Fintechs handling highly sensitive financial data, such as payment card information or personal financial records, will need the most robust and granular controls offered by adaptive zero trust.

- Existing Infrastructure: The presence of legacy systems versus a predominantly cloud-native environment will influence the ease and cost of integration.

- Budget and Resources: Adaptive zero trust often requires a higher initial investment in technology and specialized personnel, which might be a barrier for some fintechs.

Phased Implementation Strategy

Regardless of the chosen model, a phased implementation strategy is often the most effective approach. Starting with critical assets and gradually expanding the zero-trust framework across the organization allows for learning, adaptation, and minimizes disruption to operations.

This strategy also enables fintechs to demonstrate early successes, build internal support, and refine their approach based on real-world experience. Pilot programs on specific applications or departments can provide valuable insights before a full-scale rollout.

Engaging with experienced cybersecurity consultants and vendors can also provide invaluable guidance in navigating the complexities of zero-trust adoption. Their expertise can help tailor a solution that maximizes security benefits while optimizing the zero-trust fintech ROI. The ultimate goal is to build a resilient, adaptive, and cost-effective security framework that protects against the evolving threat landscape of 2025 and beyond.

| Zero-Trust Model | Key Benefit for Fintech ROI |

|---|---|

| Traditional Zero Trust | Strong foundational security with clear policy enforcement, lower initial AI/ML investment. |

| Adaptive Zero Trust | Dynamic risk assessment, real-time threat detection, reduced long-term operational costs. |

| Micro-segmentation | Contains breaches, limits lateral movement, minimizes damage and recovery time. |

| Continuous Monitoring | Proactive threat identification, faster incident response, reduced financial losses. |

Frequently Asked Questions About Zero Trust for Fintechs

Traditional zero trust relies on static, policy-driven access controls, while adaptive zero trust incorporates AI and machine learning to dynamically assess risk and adjust access policies in real-time, offering greater flexibility and responsiveness to evolving threats.

Zero trust enforces granular access controls and continuous monitoring, making it easier to demonstrate adherence to regulations like GLBA and PCI DSS. It also reduces the risk of data breaches, which helps avoid non-compliance penalties and maintains a clean regulatory record.

Essential components include robust Identity and Access Management (IAM), comprehensive device security and endpoint protection, network micro-segmentation, and continuous monitoring with advanced analytics. These elements work together to create a unified security posture.

Yes, but it can be challenging. Integration often requires a phased approach, API development, and middleware solutions to extend zero-trust principles to older infrastructure without disrupting critical operations. Careful planning is essential for successful integration.

ROI calculation involves assessing quantifiable benefits like reduced breach costs and operational efficiencies, alongside intangible gains such as enhanced customer trust and brand reputation. A thorough risk assessment and quantification of potential losses are also crucial for a comprehensive evaluation.

Conclusion

For US fintechs, the journey towards a robust cybersecurity posture in 2025 inevitably leads to zero-trust architectures. While both traditional and adaptive models offer significant advantages, the adaptive approach, with its AI-driven dynamic risk assessment and real-time policy adjustments, appears poised to deliver the superior zero-trust fintech ROI. This model not only enhances threat detection and response but also reduces long-term operational overhead, making it a strategic investment for sustained security and business growth. The path to successful implementation, however, demands careful consideration of regulatory compliance, legacy system integration, and balancing security with user experience. By embracing a phased strategy and leveraging emerging trends like AI and cloud-native security, fintechs can build a resilient defense that protects sensitive data, maintains customer trust, and secures their competitive edge in a rapidly evolving digital landscape.