The financial technology (fintech) landscape in the United States is evolving at an unprecedented pace. For startups aiming to carve out a niche and achieve sustainable growth by 2026, a meticulously planned and robust fintech tech stack is not just an advantage—it’s a fundamental necessity. The right technological foundation enables agility, scalability, security, and compliance, all while delivering an exceptional user experience. This comprehensive guide will delve into the essential platforms and considerations for building a cutting-edge fintech tech stack tailored for the US market.

Understanding the Core of a Fintech Tech Stack

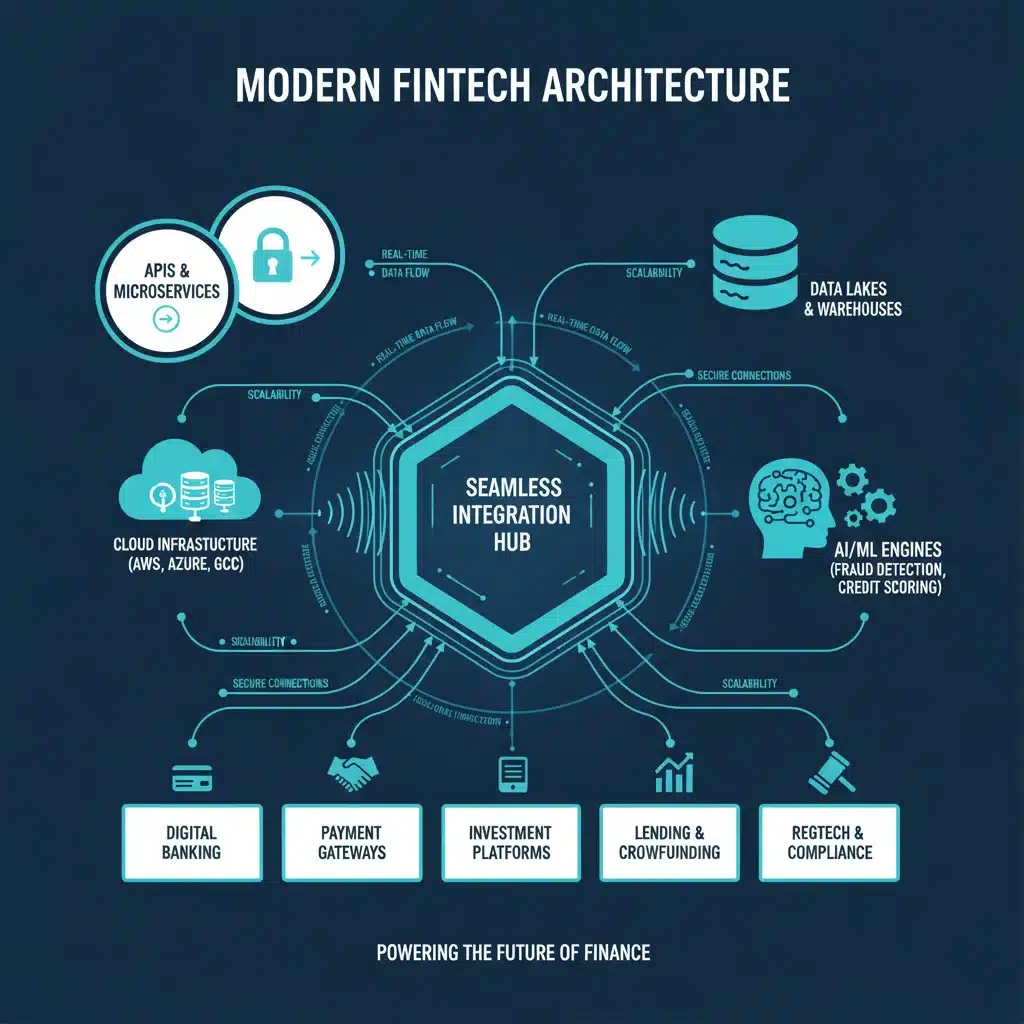

At its heart, a fintech tech stack is the combination of technologies, tools, and platforms that a financial technology company uses to build, deploy, and operate its services. This encompasses everything from programming languages and databases to cloud infrastructure, APIs, and specialized financial software. For US fintech startups, the choices made today will profoundly impact their ability to innovate, scale, and navigate the complex regulatory environment of tomorrow.

The critical components of a modern fintech tech stack can generally be categorized into several key areas:

- Core Banking & Ledger Systems: The foundational layer for all financial transactions.

- Payment Processing & Infrastructure: Enabling seamless money movement.

- Data Management & Analytics: Extracting insights and driving personalization.

- Security & Fraud Prevention: Protecting assets and user data.

- Compliance & Regulatory Technology (RegTech): Navigating complex legal frameworks.

- Customer Experience & Engagement: Building intuitive and personalized interfaces.

- Cloud Infrastructure: Providing the scalable backbone for operations.

- API Management & Integration: Connecting disparate systems and partners.

Each of these components plays a vital role in the overall health and performance of a fintech application. As we look towards 2026, the emphasis is increasingly on integrated, AI-driven, and highly secure solutions that can adapt to changing market demands and regulatory pressures.

Foundational Layer: Core Banking & Ledger Systems

For many fintechs, particularly those involved in lending, deposits, or asset management, a robust core banking or ledger system is indispensable. This is the engine that processes transactions, manages accounts, and maintains financial records. Traditional core banking systems are often monolithic and outdated, but a new generation of cloud-native and API-first solutions is transforming the landscape.

Key Considerations for Core Banking in 2026:

- Cloud-Native Architecture: Opt for platforms built from the ground up for the cloud (e.g., AWS, Azure, Google Cloud). This ensures scalability, resilience, and cost-efficiency.

- API-First Design: A strong API layer is crucial for integrating with other services, partners, and for developing new features quickly. This is a cornerstone of a flexible fintech tech stack.

- Real-time Processing: Customers expect instant transactions. Your core system must support real-time ledger updates and data availability.

- Flexibility & Configurability: The ability to easily configure products, rules, and workflows without extensive custom coding is paramount for rapid innovation.

- Regulatory Compliance Built-in: Ensure the system can handle US-specific regulations like AML, KYC, and data privacy (e.g., CCPA, state-specific requirements).

Leading Platforms & Approaches:

- Modern Core Banking Providers: Companies like Finxact, Thought Machine, and Mambu offer cloud-native, API-driven core banking solutions that are highly configurable and designed for the digital age. They allow fintechs to build custom financial products rapidly.

- Banking-as-a-Service (BaaS) Providers: For fintechs that don’t want to build a full banking infrastructure, BaaS providers (e.g., Galileo, Bond, Unit) offer modular banking services via APIs. This allows startups to embed financial products into their offerings without needing a banking license themselves. This is a powerful component of any modern fintech tech stack.

- Distributed Ledger Technology (DLT): While still maturing, DLT (blockchain) is being explored for specific ledger applications, especially for cross-border payments and asset tokenization, offering potential for enhanced transparency and efficiency.

Seamless Money Movement: Payment Processing & Infrastructure

Payments are the lifeblood of almost every fintech. Whether it’s processing credit card transactions, enabling ACH transfers, or facilitating real-time payments, the payment infrastructure must be robust, secure, and efficient. The US payment landscape is complex, with various networks and regulations.

Key Considerations for Payments in 2026:

- Multi-Channel Support: Support for various payment methods (card, ACH, wire, RTP, crypto) and channels (online, mobile, in-app).

- Fraud Detection & Prevention: Integrated, AI-powered tools to minimize fraud losses.

- Scalability & Reliability: The payment gateway must handle peak transaction volumes without downtime.

- Global Reach (if applicable): For fintechs serving international customers, cross-border payment capabilities are essential.

- Cost Efficiency: Transparent pricing models and optimized transaction fees.

- Real-Time Payments (RTP): The adoption of RTP in the US is growing, and supporting it will be a competitive differentiator.

Leading Platforms & Approaches:

- Payment Gateways & Processors: Stripe, Braintree (PayPal), and Adyen are industry leaders offering comprehensive payment processing solutions, including card acceptance, ACH, and fraud tools. They are crucial for any fintech tech stack.

- ACH & Wire Services: For direct bank transfers, working with specialized providers or leveraging BaaS platforms that offer these capabilities is common.

- Real-Time Payment Networks: Integration with The Clearing House’s RTP network or upcoming FedNow service for instant payments.

- Card Issuing Platforms: For fintechs issuing their own debit or credit cards, platforms like Marqeta or Lithic provide API-driven card issuing and program management.

Intelligent Insights: Data Management & Analytics

Data is the new oil, and in fintech, it’s the fuel for personalized experiences, risk assessment, fraud detection, and strategic decision-making. A robust data infrastructure is non-negotiable for a competitive fintech tech stack.

Key Considerations for Data in 2026:

- Data Lake/Warehouse Strategy: A centralized repository (e.g., AWS S3 for data lake, AWS Redshift or Google BigQuery for data warehouse) is essential for storing and processing vast amounts of structured and unstructured data.

- ETL/ELT Tools: Efficient tools for extracting, transforming, and loading data (e.g., Fivetran, Stitch) are needed to move data from various sources into your data repositories.

- Business Intelligence (BI) & Visualization: Tools like Tableau, Microsoft Power BI, or Looker enable teams to derive actionable insights from data.

- Machine Learning (ML) & AI Capabilities: Integration of ML platforms (e.g., AWS SageMaker, Google AI Platform) for advanced analytics, risk scoring, fraud detection, and personalized recommendations.

- Data Governance & Privacy: Strict adherence to data privacy regulations (e.g., CCPA, GDPR if applicable) and robust data governance frameworks.

Fortress-Level Protection: Security & Fraud Prevention

Security is paramount in fintech. A single breach can be catastrophic, leading to financial losses, reputational damage, and regulatory fines. Building a secure fintech tech stack requires a multi-layered approach.

Key Considerations for Security in 2026:

- End-to-End Encryption: Encrypting data at rest and in transit using industry-standard protocols.

- Multi-Factor Authentication (MFA): Implementing strong authentication mechanisms for users and internal systems.

- Identity & Access Management (IAM): Robust systems (e.g., AWS IAM, Auth0, Okta) to manage who has access to what resources.

- Fraud Detection & Prevention Systems: Utilizing AI/ML-powered systems (e.g., Sift, Forter) to identify and prevent fraudulent transactions in real-time.

- Vulnerability Management & Penetration Testing: Regular security audits, vulnerability scans, and penetration tests to identify and remediate weaknesses.

- DDoS Protection & WAF: Protecting against distributed denial-of-service attacks and common web vulnerabilities with Web Application Firewalls (WAF).

- Compliance with Security Standards: Adherence to standards like PCI DSS (if handling card data), ISO 27001, and SOC 2.

Navigating the Maze: Compliance & Regulatory Technology (RegTech)

The US financial regulatory environment is notoriously complex and constantly evolving. Fintech startups must not only comply with existing laws but also anticipate future changes. RegTech solutions are becoming an indispensable part of the fintech tech stack.

Key Considerations for RegTech in 2026:

- Know Your Customer (KYC) & Anti-Money Laundering (AML): Automated solutions for identity verification, sanctions screening, and transaction monitoring (e.g., Jumio, Onfido, Sumsub).

- Fraud & Sanctions Screening: Real-time screening against watchlists and databases to prevent illicit activities.

- Reporting & Audit Trails: Systems that automatically generate regulatory reports and maintain comprehensive audit trails for compliance.

- Data Privacy Compliance: Tools and processes to ensure compliance with data protection laws like CCPA and potential federal privacy laws.

- Automated Compliance Monitoring: Leveraging AI to monitor transactions and activities for potential compliance breaches.

Leading Platforms & Approaches:

- Identity Verification & KYC: Providers like Jumio, Onfido, and Sumsub offer robust solutions for digital identity verification, document checks, and biometric authentication.

- AML & Transaction Monitoring: Platforms such as NICE Actimize, Feedzai, and Refinitiv World-Check help in detecting suspicious activities and adhering to AML regulations.

- Regulatory Reporting: Specialized software that automates the generation and submission of regulatory reports to bodies like FinCEN, CFPB, and state regulators.

Engaging the User: Customer Experience & Engagement

Even with the most sophisticated backend, a poor user experience can lead to churn. Fintechs must prioritize intuitive design, personalized communication, and efficient customer support. This is where the frontend of the fintech tech stack comes into play.

Key Considerations for CX in 2026:

- User Interface (UI) & User Experience (UX) Design: Intuitive and aesthetically pleasing interfaces for web and mobile applications.

- Mobile-First Approach: Given the prevalence of mobile banking, a mobile-first development strategy is crucial.

- Personalization Engines: Leveraging AI/ML to offer personalized financial advice, product recommendations, and tailored communications.

- Customer Relationship Management (CRM): Systems (e.g., Salesforce, Zendesk) to manage customer interactions, support, and sales pipelines.

- Communication Channels: Integrated platforms for email, in-app messaging, chatbots, and live chat support.

- Feedback Mechanisms: Tools to collect and analyze customer feedback for continuous improvement.

The Backbone: Cloud Infrastructure

Cloud computing is no longer optional; it’s the standard for fintech. It provides the scalability, flexibility, and cost-efficiency necessary for rapid growth. The choice of cloud provider is a critical decision for any fintech tech stack.

Key Considerations for Cloud Infrastructure in 2026:

- Provider Choice: Leading providers like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP) offer comprehensive suites of services tailored for enterprise-grade applications.

- Serverless Computing: Leveraging serverless functions (e.g., AWS Lambda, Azure Functions, Google Cloud Functions) for event-driven architectures and reduced operational overhead.

- Containerization & Orchestration: Using Docker and Kubernetes for consistent deployment, scaling, and management of microservices.

- Managed Services: Opting for managed databases, message queues, and other services to reduce operational burden.

- Disaster Recovery & Business Continuity: Implementing robust strategies for data backup, replication, and rapid recovery in case of outages.

- Geographic Redundancy: Deploying services across multiple regions for high availability and disaster recovery, especially important for US-based operations.

Connecting the Ecosystem: API Management & Integration

Fintech thrives on connectivity. APIs (Application Programming Interfaces) are the glue that holds the modern fintech tech stack together, enabling seamless communication between internal systems, external partners, and third-party services.

Key Considerations for APIs in 2026:

- API Gateway: A centralized management point for all APIs, handling authentication, authorization, rate limiting, and monitoring (e.g., AWS API Gateway, Google Cloud API Gateway, Azure API Management).

- Microservices Architecture: Designing applications as a collection of loosely coupled, independently deployable services that communicate via APIs.

- Open Banking & PSD2 Compliance (if applicable): While PSD2 is European, the principles of open banking are gaining traction in the US, requiring secure and standardized API access to financial data.

- Developer Portals: Providing clear API documentation, SDKs, and sandboxes to encourage third-party developers to build on your platform.

- Security: Implementing strong API security measures, including OAuth 2.0, API keys, and comprehensive logging.

Emerging Technologies Shaping the Fintech Tech Stack

Beyond the core components, several emerging technologies are poised to significantly impact the fintech tech stack by 2026:

- Artificial Intelligence (AI) & Machine Learning (ML): Moving beyond basic analytics to predictive models for fraud, credit scoring, personalized finance, and automated customer service (chatbots).

- Blockchain & Distributed Ledger Technology (DLT): For secure, transparent, and immutable record-keeping, especially in areas like cross-border payments, supply chain finance, and digital asset management.

- Quantum Computing: While still nascent, quantum computing has the potential to revolutionize cryptography and complex financial modeling in the long term, posing both opportunities and threats.

- Embedded Finance: The integration of financial services directly into non-financial platforms, requiring robust API-driven infrastructure.

- Environmental, Social, and Governance (ESG) Tech: Tools and platforms to track, report, and manage ESG performance, becoming increasingly important for investment and regulatory compliance.

Building a Future-Proof Fintech Tech Stack: Practical Steps

For US fintech startups, the journey to a robust fintech tech stack involves strategic planning and continuous adaptation. Here are practical steps:

- Define Your Use Case & Target Market: Clearly understand your product, customer needs, and the specific regulatory landscape you operate within. This will dictate your core technology choices.

- Prioritize Security & Compliance from Day One: Integrate security and RegTech solutions into your architecture from the very beginning. Retrofitting these later is costly and risky.

- Embrace Cloud-Native & Serverless: Leverage the scalability, flexibility, and cost-efficiency of cloud services. Focus on managed services to reduce operational burden.

- Adopt an API-First Strategy: Design your systems with APIs at their core to enable seamless integration, future extensibility, and partnerships.

- Invest in Data Infrastructure: Build a robust data lake/warehouse and implement strong data governance. Data will be your competitive advantage.

- Choose Partners Wisely: Select vendors and service providers with a strong track record, regulatory expertise, and a commitment to security and innovation.

- Build for Scalability & Resilience: Design your architecture to handle exponential growth and ensure high availability and disaster recovery capabilities.

- Foster a Culture of Continuous Innovation: The fintech landscape changes rapidly. Your team and tech stack must be agile enough to adapt and innovate constantly.

- Regularly Review & Update: Technology evolves. Periodically audit your fintech tech stack to ensure it remains cutting-edge, secure, and compliant.

- Focus on User Experience: Ultimately, the best technology is one that is invisible to the user, providing a seamless, intuitive, and trustworthy experience.

Conclusion

Building a robust and future-proof fintech tech stack for US startups in 2026 is a complex yet exhilarating challenge. It requires a strategic blend of established, reliable technologies and an openness to emerging innovations. By prioritizing cloud-native architectures, API-first design, stringent security, comprehensive RegTech, and an unwavering focus on data and customer experience, fintechs can lay a solid foundation for sustained success. The right tech stack won’t just support your business; it will be the engine driving your innovation, compliance, and growth in the dynamic world of financial technology.