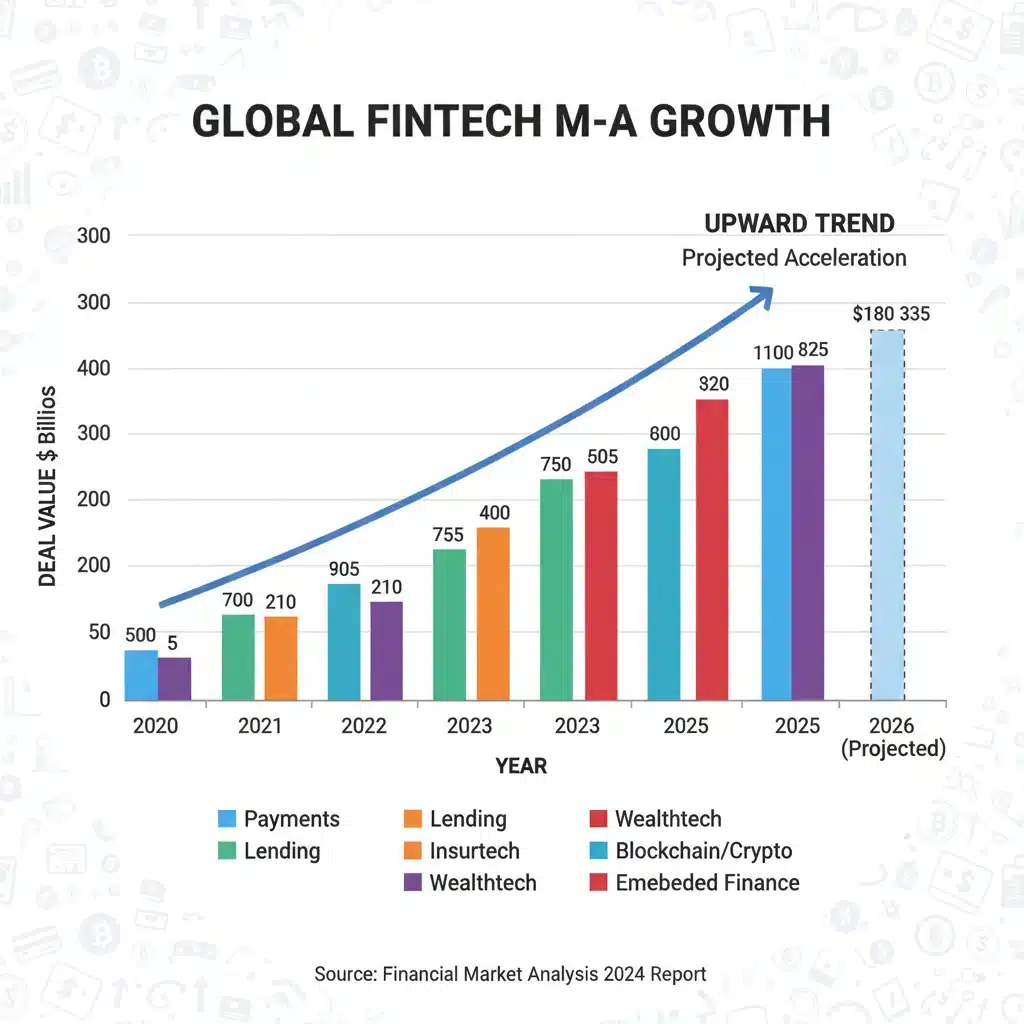

Fintech Startup Exits 2026: Acquisition Trends & Valuations in US

The financial technology (fintech) sector has been a hotbed of innovation and investment for over a decade, consistently disrupting traditional banking and financial services. As the industry matures, the focus for many investors and founders shifts towards successful exit strategies. Understanding the dynamics of Fintech Startup Exits in the US for 2026 is crucial for navigating this evolving landscape. This comprehensive analysis will delve into the anticipated acquisition trends, valuation methodologies, and the overarching factors influencing these pivotal moments for startups.

The Current State of Fintech: A Precursor to 2026 Exits

Before we project into 2026, it’s essential to understand the foundation upon which these future Fintech Startup Exits will occur. The fintech market in the US has witnessed unprecedented growth, fueled by digital transformation, changing consumer expectations, and a favorable regulatory environment (albeit with increasing scrutiny). From challenger banks and payment processors to insurtech and regtech, the innovation pipeline remains robust.

Recent years have seen a surge in venture capital funding, leading to a proliferation of fintech unicorns. However, a significant number of these startups are now reaching a stage where investors are seeking returns, and founders are looking for the next chapter. This creates a fertile ground for M&A activity and other exit opportunities. The macroeconomic climate, including interest rates and inflation, will undoubtedly play a significant role in shaping investor appetite and buyer behavior in the coming years.

Key Drivers of Fintech Growth and Exit Potential

- Digital Transformation Acceleration: The pandemic significantly accelerated the adoption of digital financial services, making them indispensable for consumers and businesses alike. This trend is unlikely to reverse, continuing to fuel demand for innovative fintech solutions.

- Embedded Finance: The integration of financial services into non-financial platforms is a powerful trend, creating new revenue streams and expanding market reach. Startups specializing in embedded finance are highly attractive acquisition targets.

- AI and Machine Learning: Advanced analytics, AI, and machine learning are revolutionizing risk assessment, fraud detection, personalized financial advice, and operational efficiency within fintech. Companies leveraging these technologies effectively are commanding higher valuations.

- Blockchain and Decentralized Finance (DeFi): While still nascent in some areas, the underlying technology of blockchain and the principles of DeFi offer transformative potential for financial infrastructure. Startups exploring these frontiers, especially in enterprise applications, are on the radar of strategic acquirers.

- Regulatory Technology (RegTech): As financial regulations become more complex, solutions that help institutions comply efficiently and effectively are in high demand. RegTech companies offer significant value proposition to larger financial institutions.

Anticipated Acquisition Trends for Fintech Startup Exits in 2026

The landscape of Fintech Startup Exits in 2026 is expected to be dynamic, characterized by several prominent acquisition trends. These trends are driven by a combination of strategic imperatives from larger corporations and the maturity cycle of many startups.

1. Strategic Acquisitions by Traditional Financial Institutions

Established banks, credit unions, and insurance companies are facing increasing pressure to innovate and modernize their offerings. Instead of building new technologies from scratch, many are opting to acquire innovative fintech startups. This strategy allows them to rapidly integrate cutting-edge technology, acquire new customer bases, and enhance their digital capabilities. We anticipate a continued focus on:

- API-first platforms: Startups offering robust APIs that can seamlessly integrate with existing legacy systems.

- Customer experience (CX) platforms: Companies that excel in creating intuitive and personalized digital experiences.

- Specialized lending platforms: Fintechs that have carved out niches in specific lending segments with efficient underwriting processes.

- Wealth management and robo-advisory: Solutions catering to a younger demographic seeking accessible and automated investment advice.

2. Consolidation within the Fintech Ecosystem

As the fintech sector matures, a natural consolidation phase is inevitable. Larger, more established fintech companies that have achieved significant market penetration and profitability will look to acquire smaller, innovative players to expand their product offerings, enter new markets, or eliminate competition. This trend will be particularly evident in crowded sub-sectors like payments, personal finance management, and business banking tools. Companies with strong unit economics and clear paths to profitability will be prime targets.

3. Tech Giants Entering the Financial Services Arena

Big tech companies (e.g., Apple, Google, Amazon, Meta) have already made inroads into financial services through payments, lending, and digital wallets. Their vast user bases, technological prowess, and deep pockets make them formidable players. We expect these tech giants to continue their strategic acquisitions of fintech startups that align with their ecosystem expansion goals, particularly those that enhance their data capabilities, customer engagement, or offer novel financial products integrated into their existing platforms.

4. Private Equity and Growth Equity Investments Turning into Exits

Private equity firms have been significant investors in fintech, often taking substantial stakes in growth-stage companies. As these investments mature, PE firms will increasingly seek exits through either IPOs (though less common for smaller exits) or strategic sales to larger corporations. This will add another layer of activity to the Fintech Startup Exits market, as these firms look to realize returns for their limited partners.

Analyzing Valuation Methodologies for Fintech Startup Exits in 2026

Valuation is a critical component of any successful exit. For fintech startups, traditional valuation methods are often adapted to account for unique characteristics such as rapid growth, recurring revenue models, and significant intellectual property. In 2026, several factors will influence how these valuations are determined.

1. Revenue Multiples Remain Dominant, with Nuances

For high-growth fintechs, revenue multiples (Enterprise Value / Revenue) will continue to be a primary valuation metric. However, the exact multiple will be heavily influenced by:

- Growth Rate: Higher, sustainable revenue growth rates will command premium multiples.

- Gross Margins: Fintechs with strong gross margins indicate a more efficient business model and better long-term profitability potential.

- Customer Acquisition Cost (CAC) & Lifetime Value (LTV): Companies demonstrating efficient customer acquisition and high customer retention will be valued more favorably.

- Recurring Revenue: A higher proportion of recurring revenue (e.g., subscriptions, transaction fees) significantly increases valuation due to predictability.

- Market Size and Penetration: The total addressable market (TAM) and the startup’s current penetration within that market are crucial.

2. Profitability and Unit Economics Gaining Importance

While growth has often been prioritized over profitability in earlier stages, the market is maturing. Investors and acquirers in 2026 will increasingly scrutinize a fintech’s path to profitability and its underlying unit economics. Startups demonstrating healthy margins, efficient operations, and a clear path to positive cash flow will be more attractive, especially in a higher interest rate environment where capital is less ‘cheap’.

3. Technology and Intellectual Property (IP) Valuation

The proprietary technology and intellectual property (e.g., patents, unique algorithms, data sets) developed by fintech startups are often their most valuable assets. Acquirers will conduct thorough due diligence to assess the defensibility, scalability, and integration potential of this IP. Startups with robust, defensible technology platforms will command higher valuations.

4. Data Assets and Network Effects

Fintech companies often accumulate significant amounts of valuable data. The ability to leverage this data for improved services, risk management, or personalized offerings adds considerable value. Furthermore, fintechs that have successfully built strong network effects (where the value of the service increases with more users) will be highly prized, as these create significant barriers to entry for competitors.

5. Regulatory Compliance and Security Infrastructure

In an increasingly regulated environment, a fintech’s compliance infrastructure and security posture are not just operational necessities but also valuation drivers. Companies with a clean regulatory record, robust cybersecurity measures, and a proactive approach to compliance will be seen as less risky and therefore more valuable targets. This mitigates potential post-acquisition liabilities for the acquirer.

Factors Influencing Successful Fintech Startup Exits in 2026

Beyond market trends and valuation methodologies, several critical factors will determine the success of Fintech Startup Exits in 2026.

1. Strong Leadership and Management Team

Acquirers don’t just buy technology; they acquire talent and leadership. A strong, experienced management team with a clear vision, proven execution capabilities, and cultural alignment with the acquiring entity can significantly enhance the attractiveness of a startup. The willingness of key founders and executives to remain post-acquisition is often a crucial negotiation point.

2. Clear Market Niche and Problem-Solving

Fintechs that effectively address a specific market pain point or serve an underserved niche tend to be more successful. Their focused approach allows for deeper expertise, stronger customer loyalty, and a clearer value proposition to potential acquirers. Solutions that offer significant cost savings, efficiency gains, or revenue generation for customers are particularly appealing.

3. Scalability and Global Potential

Acquirers look for startups with scalable business models that can grow beyond their current market. A fintech that has proven its ability to scale its operations, technology, and customer base efficiently will be more valuable. Furthermore, demonstrating potential for international expansion, even if not yet realized, can significantly increase a startup’s appeal.

4. Robust Financial Health and Forecasts

While growth is important, a clear understanding of financial health – including revenue, expenses, burn rate, and runway – is paramount. Realistic and well-substantiated financial forecasts, coupled with a history of hitting financial milestones, build trust and confidence with potential acquirers. Clean and auditable financial records are non-negotiable.

5. Competitive Landscape and Differentiation

Understanding the competitive landscape and clearly articulating a sustainable competitive advantage is vital. Whether through unique technology, superior customer experience, proprietary data, or strong brand recognition, a fintech must differentiate itself from competitors to stand out as an attractive acquisition target. This differentiation contributes directly to the defensibility of its market position and future revenue streams.

6. Regulatory Foresight and Adaptability

The regulatory environment for fintech is constantly evolving. Startups that demonstrate foresight in anticipating regulatory changes and adaptability in adjusting their business models to comply will be seen as more resilient and less risky. Proactive engagement with regulators and a strong internal compliance culture are significant assets.

The Role of Venture Capital and Private Equity in 2026 Exits

Venture Capital (VC) and Private Equity (PE) firms have been instrumental in fueling the growth of the fintech sector. In 2026, their influence on Fintech Startup Exits will be more pronounced than ever. Many startups reaching the exit stage will have VC or PE backing, and these investors will be actively seeking liquidity events.

VCs Driving Early-Stage Exits and Strategic Sales

Early-stage VCs will often push for strategic acquisitions for their portfolio companies, especially for those that may not have the scale for an IPO but have developed valuable technology or acquired a significant user base. Their networks and expertise in deal-making will be crucial in connecting startups with potential acquirers.

PE Firms Orchestrating Larger Buyouts and Consolidations

Private equity firms, with their focus on mature growth companies, will likely be involved in larger buyouts and consolidation plays. They may acquire multiple smaller fintechs to create a larger, more comprehensive platform, aiming for a significant exit down the line. Their operational expertise can also help optimize the acquired companies for greater profitability before an eventual sale.

Challenges and Considerations for Fintech Exits in 2026

While the outlook for Fintech Startup Exits in 2026 is generally positive, several challenges and considerations need to be addressed by founders and investors.

1. Valuation Expectations vs. Market Realities

The frothy valuations seen in some past funding rounds may not always translate into equally high exit valuations, especially if market conditions tighten. Founders and investors need to have realistic expectations based on current market comparables and the company’s true financial performance.

2. Integration Complexities

Post-acquisition integration can be challenging, particularly for fintechs with complex technology stacks or distinct company cultures. Acquirers will scrutinize a startup’s ability to seamlessly integrate its technology and operations, and a smooth integration plan can be a significant selling point.

3. Regulatory Scrutiny

Increased regulatory scrutiny on M&A activity, particularly in the financial sector, could lead to longer approval processes or even blockages. Antitrust concerns, data privacy regulations, and consumer protection laws will all play a role.

4. Talent Retention

Retaining key talent post-acquisition is critical for maintaining the value of the acquired company. Acquirers often offer retention bonuses and equity incentives to ensure that the intellectual capital and operational expertise remain with the combined entity.

5. Economic Headwinds

Broader economic factors, such as recessions, high interest rates, or geopolitical instability, can impact investor confidence and reduce the appetite for acquisitions. While fintech has shown resilience, it is not entirely immune to economic downturns.

Preparing for a Successful Fintech Startup Exit in 2026

For founders and investors aiming for a successful Fintech Startup Exit in 2026, proactive preparation is key. This involves a multi-faceted approach that addresses all aspects of the business.

1. Build a Strong, Sustainable Business Model

Focus on unit economics, clear revenue streams, and a path to profitability. While growth is important, sustainable growth built on a solid financial foundation is more attractive to acquirers.

2. Develop Defensible Technology and IP

Invest in R&D, secure patents where applicable, and build proprietary technology that offers a significant competitive advantage. This makes the company harder to replicate and more valuable.

3. Cultivate a Robust Customer Base and Engagement

Demonstrate strong customer acquisition, retention, and satisfaction. High LTV and low CAC are powerful indicators of a healthy business. Strong network effects further enhance this appeal.

4. Ensure Regulatory Compliance and Data Security

Proactively build a compliance framework and prioritize cybersecurity. A clean regulatory record and robust security infrastructure mitigate risks for potential acquirers.

5. Assemble an All-Star Team

Attract and retain top talent across all functions, from engineering and product to sales and marketing. A strong leadership team is a significant asset in any acquisition.

6. Prepare for Due Diligence Early

Keep financial records, legal documents, and operational data meticulously organized. A well-prepared data room can significantly streamline the due diligence process and instill confidence in buyers.

7. Engage with Advisors

Work with experienced M&A advisors, investment bankers, and legal counsel early in the process. Their expertise can help navigate complex negotiations, optimize valuation, and ensure a smooth transaction.

The Future of Fintech Exits Beyond 2026

While our focus is on 2026, the trends observed will likely set the stage for Fintech Startup Exits well into the latter half of the decade. The continuous evolution of technology, changes in consumer behavior, and shifts in the global economic landscape will ensure that the fintech M&A market remains dynamic and full of opportunities. The emphasis on profitability, sustainable growth, and innovative solutions to real-world financial problems will only intensify.

The blurring lines between traditional finance and technology will likely lead to more integrated financial ecosystems, making fintech companies with strong API capabilities and embedded finance solutions particularly valuable. Furthermore, as regulatory frameworks mature globally, companies that can navigate these complexities effectively will gain a significant advantage.

Conclusion

The year 2026 is poised to be a significant period for Fintech Startup Exits in the US. Driven by strategic acquisitions from traditional financial institutions and tech giants, as well as consolidation within the fintech sector itself, the market will offer numerous opportunities for founders and investors to realize substantial returns. Valuations will increasingly balance growth potential with profitability and robust unit economics, while defensible technology, strong leadership, and impeccable regulatory compliance will be paramount.

For those looking to capitalize on this fertile environment, meticulous preparation, a deep understanding of market trends, and strategic foresight will be the keys to unlocking successful exits. The fintech journey, from startup to exit, continues to be one of the most exciting and transformative narratives in the modern economy.