Scaling US Fintech: Achieving 50% Annual Growth by 2026

In the dynamic landscape of financial technology, the ambition to achieve significant, sustained growth is a common thread among startups. For US fintech companies, the goal of reaching 50% annual growth by 2025-2026 isn’t just a dream; it’s an attainable benchmark for those who strategically navigate the market. This comprehensive guide delves into the core strategies, challenges, and opportunities involved in scaling US fintech startups, drawing lessons from industry leaders and setting a roadmap for future success.

The fintech sector in the United States is characterized by rapid innovation, evolving regulatory frameworks, and an increasingly sophisticated consumer base. To not only survive but thrive and achieve exponential growth, startups must adopt a multifaceted approach that encompasses technological superiority, shrewd market penetration, robust risk management, and an unwavering focus on customer value. This article aims to unpack these elements, providing actionable insights for founders, investors, and industry enthusiasts alike.

Understanding the US Fintech Landscape: A Precursor to Scaling

Before diving into growth strategies, it’s crucial to understand the unique characteristics of the US fintech market. The United States boasts the largest and most diverse financial services industry globally, making it a fertile ground for fintech innovation. However, this also means intense competition, complex regulatory hurdles, and varied consumer expectations across different states and demographics.

Market Dynamics and Opportunities

The US fintech market is segmented into several key areas, including payments, lending, wealth management, insurance (insurtech), and blockchain/cryptocurrency. Each segment presents distinct opportunities and challenges. For instance, the payments sector continues to evolve with the adoption of real-time payments and embedded finance, while wealth management is being reshaped by robo-advisors and personalized financial planning tools. Identifying a specific niche and understanding its underlying dynamics is the first step towards successful scaling US fintech operations.

Demographic shifts also play a significant role. Younger generations, particularly millennials and Gen Z, are digital natives who expect seamless, mobile-first financial experiences. This demand drives innovation in user experience, personalization, and accessibility. Furthermore, underserved communities and small businesses represent significant untapped markets for fintech solutions that address traditional banking gaps.

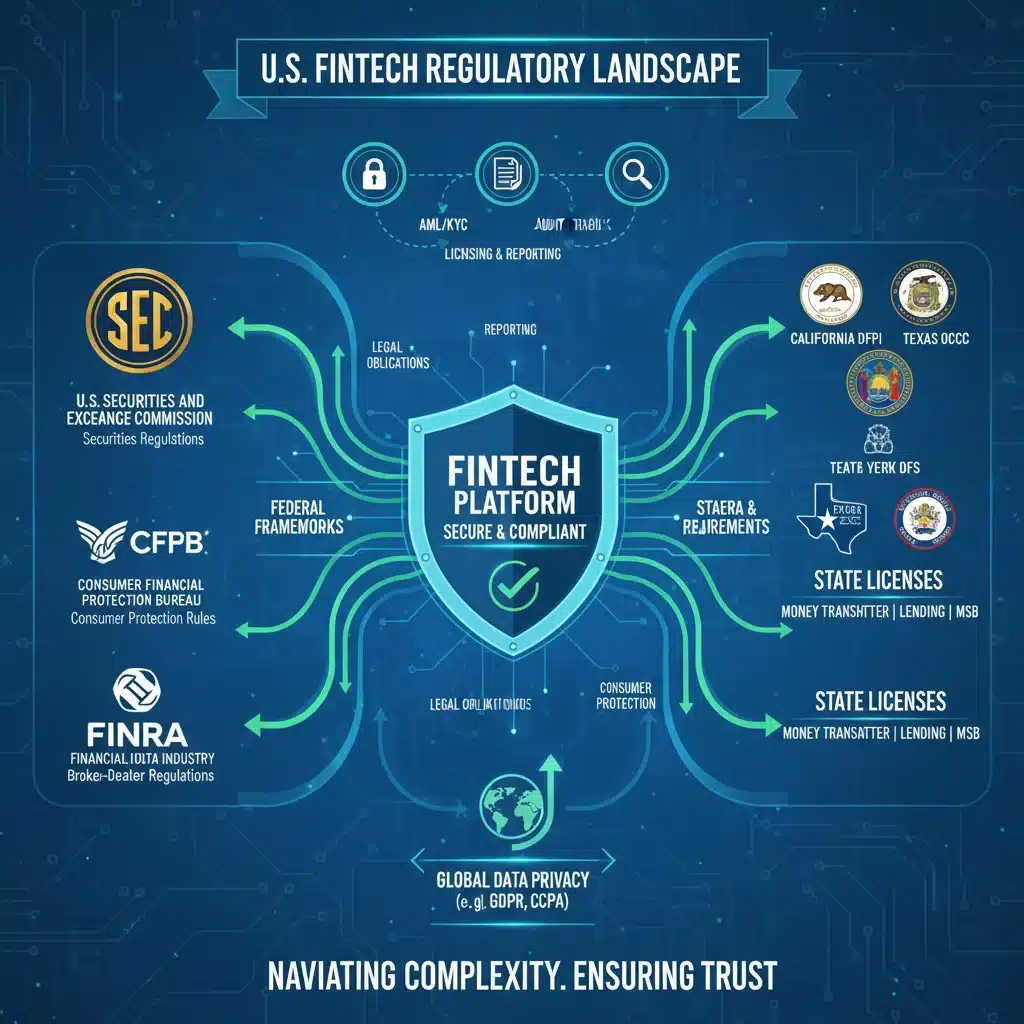

Regulatory Environment: A Double-Edged Sword

The US regulatory landscape is notoriously complex, with multiple federal and state agencies overseeing different aspects of financial services. Navigating this labyrinth requires a deep understanding of compliance requirements, including those from the Consumer Financial Protection Bureau (CFPB), the Securities and Exchange Commission (SEC), the Office of the Comptroller of the Currency (OCC), and various state banking departments. While challenging, a strong compliance framework can also be a competitive advantage, building trust and credibility with both customers and partners. Proactive engagement with regulators and investment in robust compliance technology are non-negotiable for any fintech aiming for rapid growth.

Strategic Pillars for Achieving 50% Annual Growth

Achieving aggressive growth targets like 50% annually demands a strategic, agile, and customer-centric approach. Here are the key pillars that successful US fintech companies leverage.

1. Product-Market Fit and Continuous Innovation

At the heart of any successful growth story is a compelling product that solves a real problem for a defined market segment. For fintech, this often means leveraging technology to offer services that are faster, cheaper, more accessible, or more personalized than traditional alternatives. Continuous innovation isn’t just about developing new features; it’s about constantly refining the product based on user feedback, market trends, and technological advancements.

Companies that excel in scaling US fintech understand that product-market fit is not a static state but an ongoing process. They invest heavily in R&D, data analytics to understand user behavior, and agile development methodologies to quickly iterate and deploy improvements. This allows them to stay ahead of competitors and maintain relevance in a fast-evolving market.

2. Leveraging Technology for Scalability and Efficiency

Technology is the bedrock of fintech. For rapid scaling, the underlying technological infrastructure must be robust, secure, and highly scalable. This includes cloud-native architectures, APIs for seamless integration, advanced data analytics, artificial intelligence (AI), and machine learning (ML).

- Cloud Infrastructure: Utilizing scalable cloud platforms (AWS, Azure, Google Cloud) allows fintechs to handle increased transaction volumes and user bases without significant upfront capital expenditure.

- API-First Approach: An API-first strategy enables easy integration with partners, allowing for the creation of ecosystems and expansion into new service offerings. This also facilitates embedded finance, where financial services are seamlessly integrated into non-financial platforms.

- AI and ML: These technologies are critical for personalization, fraud detection, risk assessment, and automating customer service. AI-powered insights can help identify new market opportunities and optimize operational efficiency.

- Cybersecurity: As fintechs handle sensitive financial data, robust cybersecurity measures are paramount. Investment in advanced encryption, multi-factor authentication, and continuous security audits is essential to build and maintain customer trust.

3. Strategic Partnerships and Ecosystem Building

Few fintechs can achieve hyper-growth in isolation. Strategic partnerships are often the fastest way to acquire new customers, expand service offerings, and gain access to new markets. These partnerships can take various forms:

- Banking-as-a-Service (BaaS) Providers: Collaborating with BaaS platforms allows fintechs to offer regulated financial products (e.g., deposit accounts, payment processing) without obtaining full banking licenses, significantly reducing time to market and regulatory burden.

- Incumbent Financial Institutions: While often seen as competitors, traditional banks can be valuable partners, offering access to large customer bases, established infrastructure, and regulatory expertise.

- Non-Financial Brands: Partnerships with e-commerce platforms, retailers, or tech companies can enable embedded finance solutions, reaching customers at their point of need.

- Technology Vendors: Collaborating with specialized technology providers for areas like fraud detection, compliance, or customer engagement can enhance product capabilities and operational efficiency.

4. Customer Acquisition and Retention Strategies

Aggressive growth requires a sophisticated approach to customer acquisition and retention. For scaling US fintech startups, this involves:

- Data-Driven Marketing: Utilizing data analytics to identify target demographics, personalize marketing messages, and optimize campaign performance across various channels (digital, social, content marketing).

- Referral Programs: Leveraging existing customer satisfaction to drive organic growth through well-designed referral programs.

- Exceptional Customer Experience (CX): In a crowded market, CX is a key differentiator. Providing intuitive user interfaces, responsive customer support, and personalized services builds loyalty and reduces churn.

- Community Building: Fostering a sense of community around the product, especially for niche fintechs, can lead to strong brand advocacy and organic growth.

5. Navigating the Regulatory Labyrinth and Ensuring Compliance

Regulation is not merely a hurdle but a foundational element for sustainable growth in fintech. Failure to comply can lead to hefty fines, reputational damage, and even business closure. Proactive regulatory engagement is vital.

- Early Legal Counsel: Engaging experienced legal and compliance professionals from the outset can save significant time and resources down the line.

- Compliance by Design: Integrating compliance requirements into the product development lifecycle, rather than as an afterthought.

- State-by-State Licensing: Understanding and securing necessary state licenses (e.g., money transmitter licenses, lending licenses) is crucial for nationwide expansion.

- Data Privacy and Security: Adhering to data privacy regulations (e.g., California Consumer Privacy Act CCPA, Gramm-Leach-Bliley Act GLBA) and investing in robust cybersecurity infrastructure is non-negotiable.

Case Studies: Lessons from High-Growth US Fintechs

Examining companies that have successfully achieved rapid growth offers invaluable insights. While specific names might change, the underlying principles remain consistent.

Example 1: The Neobank Disruptor

A prominent US neobank achieved over 70% annual growth for several years by focusing on underserved demographics and offering a superior mobile-first banking experience. Their strategy included:

- Hyper-personalization: AI-driven financial insights and budgeting tools tailored to individual user spending habits.

- Fee-Free Model: Eliminating common banking fees, which resonated strongly with their target market.

- Strategic Partnerships: Collaborating with established banks for FDIC insurance and payment networks, while maintaining a lean, tech-driven operational model.

- Community Engagement: Building a strong online community and leveraging social media for customer support and brand building.

Example 2: The Lending Innovator

A fintech lender specializing in small business loans witnessed significant growth by leveraging alternative data sources and AI for faster, more accurate credit assessments. Their success factors included:

- Proprietary Algorithms: Developing advanced ML models to assess creditworthiness beyond traditional FICO scores, opening up lending to a broader pool of businesses.

- Streamlined Application Process: Offering fully digital, quick application and approval processes, addressing a key pain point for small businesses.

- Focused Niche: Initially targeting specific industries with high growth potential but often overlooked by traditional lenders.

- Scalable Technology: Investing in a highly automated loan origination and servicing platform that could handle rapidly increasing volumes.

Overcoming Challenges in Scaling US Fintech

Growth is rarely linear. Fintechs aiming for 50% annual growth will inevitably face significant challenges.

Talent Acquisition and Retention

The demand for skilled fintech professionals – engineers, data scientists, compliance officers, and product managers with financial expertise – far outstrips supply. Attracting and retaining top talent requires competitive compensation, a strong company culture, opportunities for professional development, and a compelling mission.

Funding and Capital Management

While venture capital flows into fintech remain robust, securing successive rounds of funding requires demonstrating clear milestones and a path to profitability. Efficient capital management, understanding burn rates, and strategically allocating resources are crucial for sustaining growth without running out of runway.

Market Saturation and Competition

The US fintech market is becoming increasingly crowded. Differentiating a product or service, maintaining a competitive edge, and responding to new entrants are ongoing challenges. This reinforces the need for continuous innovation, superior customer experience, and strategic partnerships.

Technological Debt

Rapid development can sometimes lead to technological debt – a codebase that is difficult to maintain or scale. Proactive management of tech debt, regular refactoring, and adherence to best practices in software engineering are vital to ensure long-term scalability and agility.

The Road Ahead: Future Trends Impacting Scaling US Fintech

Looking towards 2025-2026 and beyond, several trends will continue to shape the strategies for scaling US fintech startups.

Embedded Finance Everywhere

The integration of financial services directly into non-financial platforms will become even more pervasive. Fintechs that can seamlessly embed their offerings into the customer journeys of other industries (e.g., e-commerce, healthcare, automotive) will unlock massive growth potential.

Decentralized Finance (DeFi) and Web3 Integration

While still nascent and highly regulated, DeFi and Web3 technologies (blockchain, smart contracts, cryptocurrencies) hold the promise of transforming financial infrastructure. Fintechs that can responsibly and compliantly integrate these technologies, particularly for cross-border payments, asset tokenization, or new lending models, could gain a significant advantage.

Hyper-Personalization and AI-Driven Insights

The ability to offer truly personalized financial advice, products, and experiences will deepen. AI and ML will move beyond basic recommendations to predictive analytics, helping customers make better financial decisions and optimizing product offerings in real-time.

ESG (Environmental, Social, and Governance) Focus

Consumers and investors are increasingly prioritizing ESG factors. Fintechs that integrate sustainable practices, offer socially responsible investment options, or promote financial inclusion will resonate strongly with a growing segment of the market.

Regulatory Sandboxes and Innovation Charters

Regulators are slowly adapting to the pace of fintech innovation. The proliferation of regulatory sandboxes and innovation charters at both federal and state levels will provide fintechs with clearer pathways to test new products and services in a controlled environment, potentially accelerating time to market for innovative solutions.

Building a Growth-Oriented Culture

Beyond strategy and technology, the culture within a fintech startup is paramount for achieving and sustaining high growth. A growth-oriented culture is characterized by:

- Agility and Adaptability: The ability to quickly pivot, learn from failures, and adapt to changing market conditions.

- Customer Obsession: A deep-seated commitment to understanding and serving customer needs, placing the customer at the center of all decisions.

- Data-Driven Decision Making: Relying on metrics and analytics to inform strategy, product development, and operational improvements.

- Innovation Mindset: Encouraging experimentation, creative problem-solving, and continuous improvement across all teams.

- Collaboration: Fostering an environment where cross-functional teams work seamlessly together to achieve common goals.

Investing in employee training, promoting transparency, and recognizing achievements are also critical components of building a culture that can support aggressive growth targets. A highly motivated and aligned team is arguably the most valuable asset for any startup aiming to conquer the market.

Conclusion: The Path to 50% Annual Growth is Paved with Strategy and Execution

Achieving 50% annual growth for US fintech startups by 2025-2026 is an ambitious yet achievable goal. It demands a clear vision, a robust product-market fit, scalable technology, strategic partnerships, and an unwavering commitment to regulatory compliance and customer experience. The US market, with its size and complexity, offers immense opportunities for those who are prepared to innovate, adapt, and execute flawlessly.

The lessons from successful fintechs underscore the importance of understanding the unique regulatory nuances, embracing an API-first approach, and leveraging AI for competitive advantage. As the fintech landscape continues to evolve, companies that prioritize continuous innovation, foster a strong growth culture, and strategically navigate the challenges will be best positioned to not only meet but exceed these ambitious growth targets. The journey of scaling US fintech is challenging, but for those who master its intricacies, the rewards are substantial. The next few years promise to be transformative for the financial services industry, and fintech startups are at the forefront of this revolution.