Fintech MFA: Advanced Security Strategies for 2026

The financial technology (Fintech) landscape is a dynamic and ever-evolving arena, characterized by rapid innovation and an increasing reliance on digital platforms. As financial services become more accessible and integrated into our daily lives, the imperative for robust security measures has never been more critical. Traditional password-based authentication, once the cornerstone of digital security, is now widely recognized as insufficient against the sophisticated cyber threats of today. This realization has propelled Multi-Factor Authentication (MFA) to the forefront of cybersecurity discussions, particularly within the Fintech sector. However, as we look towards 2026, even the standard forms of MFA are beginning to show their limitations. The future of Fintech security demands a proactive and comprehensive approach, moving beyond conventional MFA implementations to embrace advanced strategies that not only fortify defenses but also enhance the user experience.

The stakes in Fintech are exceptionally high. Breaches of financial data can lead to monumental financial losses, severe reputational damage, and a complete erosion of customer trust. Regulators worldwide are tightening their grip, imposing stricter compliance requirements and hefty penalties for security failures. In this environment, Fintech companies must not merely react to threats but anticipate them, building security architectures that are resilient, adaptable, and forward-looking. This article delves into the advanced strategies for implementing Multi-Factor Authentication in Fintech by 2026, exploring how organizations can move beyond simple passwords and even basic MFA to cultivate a truly secure and seamless financial ecosystem.

The Evolving Threat Landscape in Fintech

Before diving into advanced Fintech MFA Security strategies, it’s crucial to understand the threats they are designed to counter. The cyber threat landscape is a moving target, constantly shifting with new attack vectors and increasingly sophisticated adversaries. For Fintech, this landscape is particularly treacherous due to the valuable data held and the direct financial implications of a breach. Phishing, social engineering, malware, and credential stuffing attacks continue to be prevalent, but their methods are becoming more refined and harder to detect.

Phishing attacks, for instance, are no longer just generic emails; they are highly targeted spear-phishing campaigns that mimic legitimate communications from trusted financial institutions. Social engineering exploits human psychology, manipulating individuals into revealing sensitive information or granting unauthorized access. Malware, including ransomware and spyware, can compromise entire systems, leading to data exfiltration or operational paralysis. Credential stuffing, where attackers use stolen credentials from one service to try and access others, remains a significant threat, especially given the common practice of password reuse among users. These threats underscore the inadequacy of passwords alone and highlight the urgent need for more robust authentication mechanisms.

Beyond these traditional threats, emerging challenges also demand attention. The proliferation of IoT devices in financial services, the increasing complexity of supply chains, and the adoption of cloud-native architectures introduce new vulnerabilities. Nation-state actors and organized cybercrime groups are continuously developing new techniques, making it imperative for Fintech organizations to adopt a defense-in-depth strategy, with advanced authentication at its core. The goal is not just to prevent unauthorized access but to establish a continuous trust assessment throughout the user journey, making initial access incredibly difficult and subsequent unauthorized actions virtually impossible without detection.

Limitations of Traditional MFA in Fintech

While traditional MFA, which typically involves a password combined with a one-time passcode (OTP) via SMS or an authenticator app, has significantly improved security compared to passwords alone, it’s not without its drawbacks, especially in the context of advanced Fintech operations. These limitations become more apparent as we consider the scalability, user experience, and evolving threat landscape that Fintech companies face.

One of the primary weaknesses of SMS-based OTPs is their susceptibility to SIM-swapping attacks. In a SIM-swapping attack, criminals trick mobile carriers into transferring a victim’s phone number to a new SIM card under their control. Once they control the phone number, they can intercept OTPs and bypass MFA. While less common, this type of attack can be devastating, making SMS OTPs a less secure option for high-value financial transactions. Authenticator apps are generally more secure than SMS, as they are not tied to the phone number directly, but they can still be vulnerable to phishing if users are tricked into entering codes on malicious sites.

Furthermore, traditional MFA can sometimes introduce friction into the user experience. Requiring users to constantly switch between apps or wait for SMS codes can be cumbersome, leading to user frustration and potentially impacting adoption rates. In the fast-paced world of Fintech, where convenience is often a key differentiator, a clunky authentication process can deter users. The challenge, therefore, is to implement Fintech MFA Security that is both highly secure and remarkably seamless, striking a delicate balance between protection and usability. This necessitates exploring methods that integrate more organically into the user’s workflow, reducing explicit authentication steps while maintaining a high level of assurance.

Another critical limitation is the ‘human factor.’ Even with MFA, users can be tricked into approving fraudulent transactions or revealing their authentication codes through sophisticated social engineering. This highlights that technology alone is not a panacea; a comprehensive security strategy must also include user education and awareness programs. However, advanced MFA techniques aim to minimize the impact of human error by introducing factors that are harder to compromise through social engineering, such as biometrics or physical security keys.

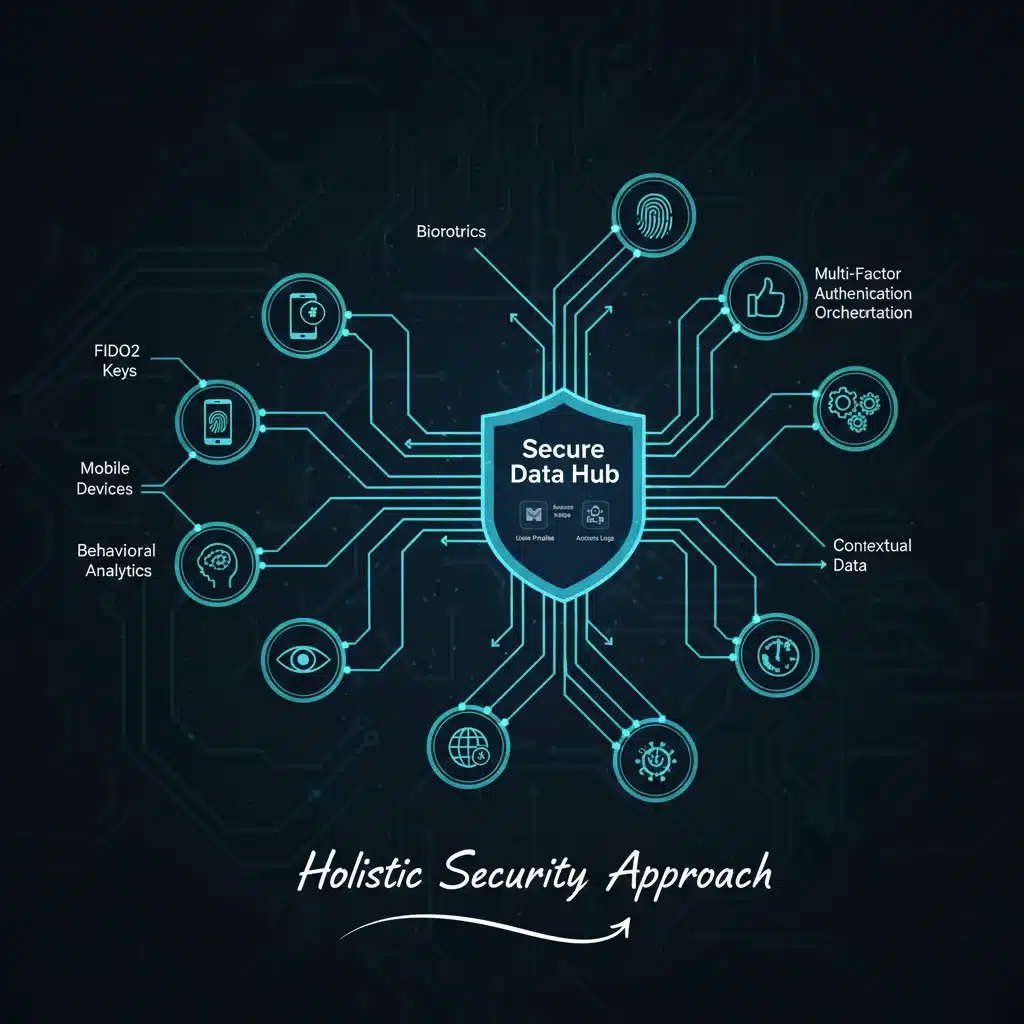

Advanced Fintech MFA Strategies for 2026

As we move towards 2026, the focus for Fintech MFA Security shifts towards more sophisticated, adaptive, and user-friendly authentication methods. These strategies aim to not only strengthen security postures but also to provide a frictionless experience that encourages adoption and enhances trust.

1. Biometric Authentication: The Human Factor as a Key

Biometrics leverage unique biological or behavioral characteristics for authentication, offering a highly secure and convenient alternative to passwords. In 2026, we anticipate a significant increase in the adoption of advanced biometric modalities within Fintech.

- Fingerprint Scanning: Already common, but advancements in sensor technology and liveness detection will make it even more robust against spoofing attempts. Integrated sensors in smartphones and dedicated hardware will continue to improve accuracy and speed.

- Facial Recognition: Technologies like Apple’s Face ID, which use 3D mapping, are far more secure than traditional 2D facial recognition. Future implementations will incorporate even more sophisticated liveness detection to prevent spoofing with photos or videos.

- Iris and Retina Scanning: Offering extremely high accuracy, these methods are gaining traction for high-security transactions. The uniqueness of iris patterns makes them ideal for environments requiring maximum assurance.

- Voice Recognition: While still evolving, voice biometrics can be used for authentication, especially when combined with other factors. Advanced systems can detect subtle variations in voice patterns and even differentiate between live speech and recordings.

- Vein Pattern Recognition: This highly secure method scans the unique patterns of blood vessels beneath the skin, which are nearly impossible to forge. It’s gaining popularity for high-security applications due to its accuracy and resistance to spoofing.

The key to successful biometric implementation lies in secure enrollment, robust liveness detection, and the protection of biometric templates. These templates must be stored securely, often encrypted and tokenized, to prevent their compromise. Furthermore, biometric authentication should ideally be combined with another factor, such as device possession or a PIN, to achieve true multi-factor assurance.

2. Passwordless Authentication with FIDO2

The FIDO (Fast Identity Online) Alliance has been instrumental in developing standards for passwordless authentication, and FIDO2 is at the forefront of this movement. FIDO2 allows users to authenticate using strong cryptographic credentials that are stored on a secure authenticator (e.g., a security key, a smartphone with a built-in authenticator, or a biometric device). This eliminates the need for passwords entirely, significantly reducing the risk of phishing, credential stuffing, and other password-related attacks.

How FIDO2 works:

- Public Key Cryptography: When a user registers with a service, their FIDO2 authenticator generates a unique public/private key pair. The public key is sent to the service provider, while the private key remains securely on the authenticator.

- Authentication: To log in, the service provider sends a challenge to the user’s authenticator. The authenticator uses its private key to sign the challenge, and this signed challenge is sent back to the service provider, which verifies it with the stored public key.

- User Verification: The user interacts with the authenticator (e.g., by touching a security key, entering a PIN, or using a biometric scan) to authorize the signing operation. This provides the ‘something you have’ and ‘something you are’ factors.

FIDO2 offers significant advantages for Fintech MFA Security:

- Phishing Resistance: Because FIDO2 relies on cryptographic proofs and origin binding, it’s inherently resistant to phishing. Users cannot be tricked into sending their credentials to a malicious site.

- Improved User Experience: Eliminating passwords simplifies the login process, making it faster and less frustrating for users.

- Strong Security: The use of public-key cryptography provides a high level of assurance, making it extremely difficult for attackers to compromise.

- Standardization: As an open standard, FIDO2 promotes interoperability across various devices and services.

Implementing FIDO2 requires careful planning, including integration with existing identity management systems and user education. However, the long-term benefits in terms of security and user satisfaction make it a compelling strategy for Fintech in 2026.

3. Behavioral Biometrics and Continuous Authentication

Behavioral biometrics analyzes unique patterns in how users interact with their devices, such as keystroke dynamics, mouse movements, scrolling patterns, and even gait patterns (if using mobile devices with accelerometers). This creates a ‘digital fingerprint’ of user behavior that can be used for continuous authentication.

- Passive and Continuous: Unlike explicit authentication methods, behavioral biometrics operate in the background, continuously verifying the user’s identity throughout a session. If a deviation from the established behavioral profile is detected, it can trigger step-up authentication or flag the session for review.

- Fraud Detection: This approach is particularly effective in detecting account takeover attempts, even if an attacker manages to bypass initial MFA. If the user’s typing rhythm, navigation patterns, or even the way they hold their phone deviates significantly from their norm, the system can flag it as suspicious.

- Reduced Friction: By continuously authenticating users passively, behavioral biometrics can reduce the need for frequent explicit authentication prompts, leading to a smoother user experience without compromising security.

Implementing behavioral biometrics for Fintech MFA Security requires advanced machine learning and artificial intelligence algorithms to build and maintain accurate user profiles. It also necessitates a robust data collection and analysis infrastructure. However, the ability to provide real-time, adaptive security makes it an invaluable tool for preventing sophisticated fraud.

4. Adaptive and Context-Aware Authentication

Adaptive authentication, also known as risk-based authentication, dynamically adjusts the level of authentication required based on the context of the access attempt. This moves beyond a one-size-fits-all approach, applying stronger authentication only when necessary, thereby improving both security and user convenience.

Factors considered in adaptive authentication include:

- Location: Is the user logging in from an unusual geographical location?

- Device: Is it a recognized device, or a new, unregistered one?

- Time of Day: Is the access attempt outside typical working hours or unusual for the user?

- Network: Is the user connecting from a known secure network or an unfamiliar public Wi-Fi?

- Transaction Value/Risk: Is the user attempting a high-value transaction or a sensitive data access?

- Historical Behavior: Does the current activity deviate from the user’s established patterns?

By analyzing these contextual indicators in real-time, adaptive authentication systems can make intelligent decisions. For low-risk activities, a simple biometric scan might suffice. For high-risk transactions, such as transferring large sums of money or changing account details, the system might demand multiple factors, including a FIDO2 key and a biometric verification. This intelligent approach optimizes both security and usability, making it a cornerstone of advanced Fintech MFA Security for 2026.

5. Decentralized Identity and Self-Sovereign Identity (SSI)

While still in nascent stages of widespread adoption, decentralized identity and Self-Sovereign Identity (SSI) hold immense promise for the future of authentication in Fintech. SSI empowers individuals with control over their digital identities, moving away from centralized identity providers. Built on blockchain technology, SSI allows users to store their verifiable credentials (e.g., proof of identity, financial qualifications) in a secure digital wallet, and selectively present them to service providers without revealing unnecessary personal information.

In an SSI model, instead of relying on a Fintech company to verify identity through third-party services, users can present cryptographically verifiable claims directly from their digital wallet. This can significantly streamline onboarding processes, reduce fraud, and enhance privacy. For Fintech MFA Security, SSI could mean that instead of authenticating with a traditional username/password combo and an MFA token, users could present a verifiable credential from their digital wallet proving their identity, combined with a biometric signature.

Key benefits of SSI for Fintech:

- Enhanced Privacy: Users share only the necessary information, reducing data exposure.

- Reduced Fraud: Verifiable credentials are cryptographically secure and tamper-proof.

- Improved User Experience: Streamlined onboarding and authentication processes.

- Greater Control: Users own and manage their digital identities.

While the infrastructure for widespread SSI adoption is still developing, Fintech companies should closely monitor this space and consider pilot programs, as it represents a paradigm shift in digital identity and authentication.

Integrating Advanced MFA into the Fintech Ecosystem

Implementing these advanced Fintech MFA Security strategies is not a trivial task. It requires careful planning, robust infrastructure, and a clear understanding of both technical capabilities and user needs. Integration into existing systems is a primary challenge, as legacy systems may not be designed to accommodate these new authentication paradigms. Fintech companies must prioritize interoperability, ensuring that new MFA solutions can seamlessly integrate with their core banking systems, payment gateways, and other critical applications.

A phased approach to implementation is often advisable. Starting with pilot programs for specific high-risk transactions or a subset of users can help identify potential issues and gather user feedback before a wider rollout. Training for both internal staff and customers is also crucial. Users need to understand the benefits of these new authentication methods and how to use them effectively. Clear communication about the security advantages and ease of use can drive adoption and minimize resistance to change.

Furthermore, Fintech companies must consider the regulatory landscape. Different jurisdictions have varying requirements for customer authentication and data privacy. Any advanced MFA strategy must be designed with compliance in mind, ensuring that it meets or exceeds standards set by bodies like the GDPR, PSD2, and various national financial regulators. Regular audits and assessments of the MFA infrastructure are essential to ensure ongoing compliance and to identify any vulnerabilities that may emerge.

The choice of advanced MFA solutions should also align with the company’s specific risk profile and target audience. For instance, a Fintech serving a tech-savvy demographic might find greater success with FIDO2 keys and biometric facial recognition, while a platform catering to a broader, less tech-oriented audience might need to introduce these technologies more gradually, perhaps starting with simpler biometric options and strong adaptive authentication.

Another critical aspect is the development of a strong identity and access management (IAM) framework. Advanced MFA solutions are most effective when integrated into a comprehensive IAM strategy that covers the entire identity lifecycle, from provisioning and de-provisioning to access governance and audit trails. This holistic approach ensures that authentication is not just a standalone security measure but an integral part of an overarching security posture.

The Future of Fintech MFA Security: AI and Quantum Resistance

Looking beyond 2026, the evolution of Fintech MFA Security will likely be driven by two major technological advancements: artificial intelligence (AI) and the impending threat of quantum computing.

AI and machine learning will play an increasingly significant role in enhancing adaptive authentication and behavioral biometrics. More sophisticated AI models will be able to analyze vast amounts of data in real-time, detecting subtle anomalies that indicate fraudulent activity with greater accuracy and speed. This will lead to truly dynamic authentication systems that can predict and prevent attacks before they even fully materialize. AI could also be used to personalize authentication challenges, making them more relevant and less intrusive for legitimate users, while posing greater hurdles for attackers.

The rise of quantum computing poses a long-term, but potentially catastrophic, threat to current cryptographic standards. Many of the encryption algorithms that underpin digital security, including those used in FIDO2 and other advanced MFA solutions, could theoretically be broken by powerful quantum computers. While fully functional quantum computers capable of this are still some years away, Fintech companies must start planning for post-quantum cryptography (PQC).

Developing and implementing quantum-resistant MFA solutions will be a critical challenge. This will involve researching and adopting new cryptographic algorithms that are secure against quantum attacks. Standard bodies and industry consortia are already working on PQC standards, and Fintech organizations should actively participate in these discussions and begin to strategize how they will transition their security infrastructure to a quantum-safe state. This foresight will ensure that their advanced MFA strategies remain robust against future threats.

Furthermore, the convergence of different authentication technologies will become more pronounced. We will see seamless integration of biometrics, FIDO2, behavioral analytics, and potentially even new modalities like brain-computer interfaces (BCI) or augmented reality (AR) for authentication in specialized contexts. The goal will be to create an invisible, yet impenetrable, layer of security that operates effortlessly in the background, making unauthorized access virtually impossible without disrupting the legitimate user experience.

Conclusion: Securing the Fintech Frontier

The journey towards advanced Fintech MFA Security is a continuous one, driven by innovation, evolving threats, and the relentless pursuit of a seamless user experience. As we approach 2026, the imperative to move beyond traditional passwords and even basic MFA strategies is undeniable. Biometric authentication, passwordless FIDO2, behavioral biometrics, adaptive authentication, and the exploration of decentralized identity represent the cutting edge of this evolution.

Fintech companies that embrace these advanced strategies will not only fortify their defenses against sophisticated cyber threats but also build greater trust with their customers, differentiate themselves in a competitive market, and comply with increasingly stringent regulatory requirements. The future of financial technology hinges on its ability to provide both innovation and unwavering security. By strategically implementing these advanced MFA solutions, Fintech organizations can secure the digital frontier, safeguarding assets, identities, and the very foundation of digital finance for years to come. The investment in these advanced security measures is not an expense, but an essential strategic imperative, ensuring resilience and fostering innovation in an increasingly connected and challenging world.