Securing Digital Payment Infrastructures: Best Practices for US Fintechs in 2026

The landscape of digital payments is evolving at an unprecedented pace, driven by technological advancements and shifting consumer expectations. For US Fintechs, this dynamic environment presents immense opportunities but also significant challenges, particularly concerning the security of their digital payment infrastructures. As we look towards 2026, the need for robust, proactive, and resilient security measures has never been more critical. The increasing sophistication of cyber threats, coupled with an ever-tightening regulatory framework, demands that Fintechs prioritize and continuously enhance their Fintech Payment Security strategies.

In this comprehensive guide, we will delve into the essential best practices that US Fintechs must adopt to safeguard their digital payment systems. We’ll explore everything from foundational security principles to cutting-edge technologies, regulatory compliance, and the human element of security. Our aim is to provide a roadmap for Fintechs to not only meet but exceed the security demands of the future, ensuring trust, integrity, and sustained growth in the digital economy.

The Evolving Threat Landscape for Fintech Payment Security

Before diving into solutions, it’s crucial to understand the threats. Cybercriminals are constantly innovating, employing sophisticated techniques to exploit vulnerabilities in digital payment systems. For US Fintechs, this means facing a diverse array of potential attacks:

- Phishing and Social Engineering: These remain primary attack vectors, targeting employees and customers to gain unauthorized access to sensitive information.

- Malware and Ransomware: Malicious software designed to disrupt operations, steal data, or extort money continues to pose a significant threat.

- Distributed Denial-of-Service (DDoS) Attacks: These attacks can cripple payment processing capabilities, leading to significant financial losses and reputational damage.

- API Vulnerabilities: As Fintechs increasingly rely on APIs for connectivity and service delivery, unsecured APIs become a prime target for data breaches.

- Insider Threats: Malicious or negligent actions by employees can lead to data compromise or system disruption.

- Supply Chain Attacks: Exploiting vulnerabilities in third-party vendors and partners to gain access to a Fintech’s systems.

- Identity Theft and Account Takeover (ATO): Sophisticated methods to assume a user’s identity and gain control over their financial accounts.

The financial sector is a prime target due to the high value of data and transactions. Therefore, a multi-faceted approach to Fintech Payment Security is not just advisable, but absolutely essential for survival and prosperity in the competitive Fintech space.

Foundational Pillars of Robust Fintech Payment Security

Building a secure digital payment infrastructure requires a strong foundation. These pillars are non-negotiable for any US Fintech aiming for long-term success and resilience:

1. Comprehensive Risk Assessment and Management

A continuous, systematic approach to identifying, assessing, and mitigating risks is the bedrock of effective Fintech Payment Security. This involves:

- Regular Vulnerability Assessments and Penetration Testing: Proactively identify weaknesses in systems, applications, and networks before malicious actors do.

- Threat Modeling: Analyze potential threats and design security controls to counter them.

- Business Impact Analysis: Understand the potential financial and reputational impact of various security incidents.

- Incident Response Planning: Develop and regularly test a clear, actionable plan for responding to security breaches.

2. Strong Authentication and Authorization Mechanisms

Identity is the new perimeter. Robust authentication and authorization are paramount for protecting access to sensitive systems and data:

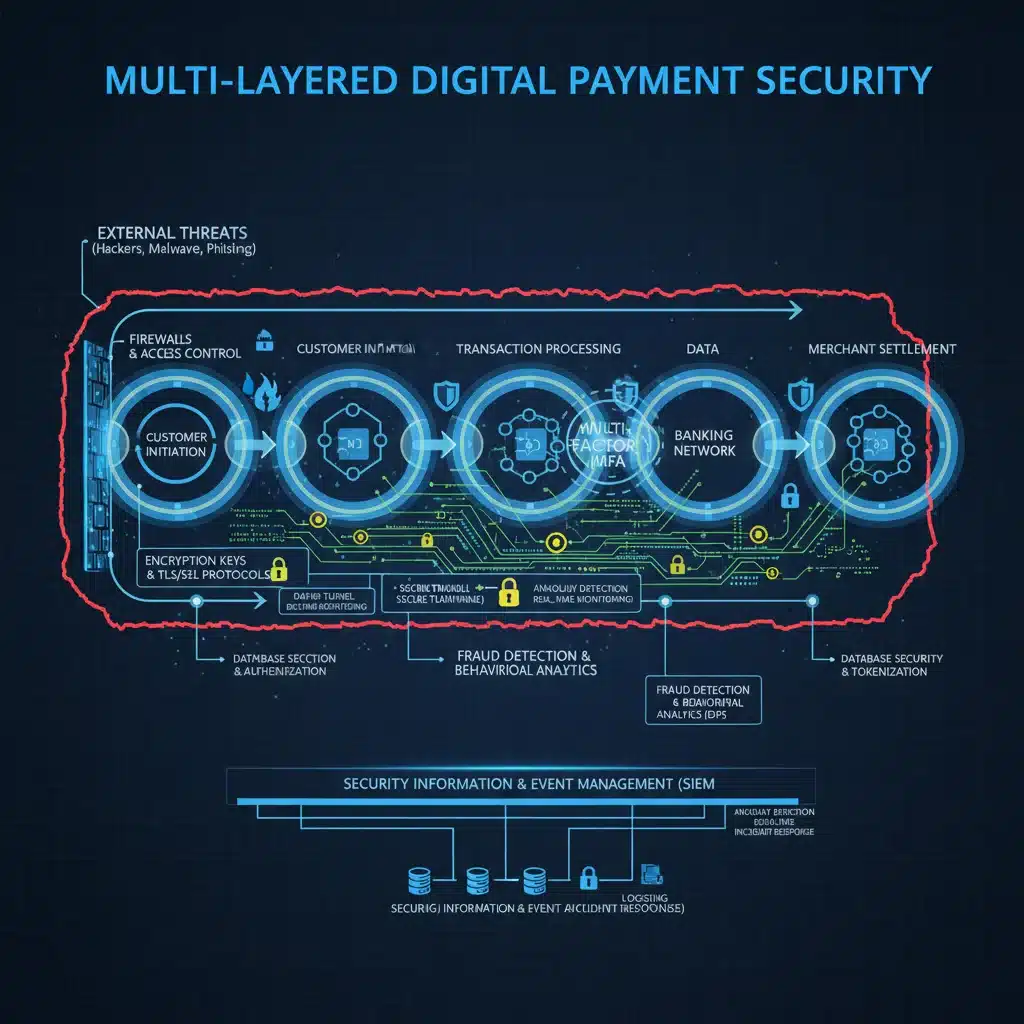

- Multi-Factor Authentication (MFA): Implement MFA for all internal and external users accessing payment systems. This adds an extra layer of security beyond just passwords.

- Biometric Authentication: Leverage technologies like fingerprint, facial, or iris recognition for enhanced user verification, especially in mobile payment applications.

- Access Control (RBAC/ABAC): Implement Role-Based Access Control (RBAC) or Attribute-Based Access Control (ABAC) to ensure users only have access to the resources absolutely necessary for their job functions (principle of least privilege).

- Session Management: Securely manage user sessions to prevent unauthorized access.

3. Data Encryption and Tokenization

Protecting data at rest and in transit is fundamental. Encryption and tokenization are key technologies:

- End-to-End Encryption: Encrypt all sensitive data, from customer input to storage and transmission. This includes data in databases, cloud environments, and communication channels.

- Tokenization: Replace sensitive payment card data with unique, non-sensitive tokens. This significantly reduces the scope of PCI DSS compliance and minimizes the impact of a data breach.

- Hardware Security Modules (HSMs): Utilize HSMs for secure key management and cryptographic operations, ensuring the integrity of encryption processes.

4. Secure Software Development Lifecycle (SSDLC)

Security must be baked into the development process, not bolted on afterwards. An SSDLC integrates security practices at every stage:

- Security Requirements: Define security requirements from the outset of any project.

- Secure Coding Practices: Train developers in secure coding standards and conduct regular code reviews.

- Automated Security Testing: Integrate Static Application Security Testing (SAST) and Dynamic Application Security Testing (DAST) into CI/CD pipelines.

- Third-Party Component Management: Scrutinize and secure all third-party libraries and components used in applications.

Navigating the Regulatory Landscape: Compliance in 2026

For US Fintechs, compliance with a complex web of regulations is not optional; it’s a legal and ethical imperative. Non-compliance can lead to severe penalties, reputational damage, and loss of customer trust. As of 2026, key regulations and standards impacting Fintech Payment Security include:

1. Payment Card Industry Data Security Standard (PCI DSS)

Any Fintech handling credit card data must comply with PCI DSS. This standard sets forth requirements for securing payment card data through controls like network security, data protection, vulnerability management, and access control. While PCI DSS v4.0 offers more flexibility and a future-proof approach, continuous adherence and regular audits are critical.

2. Gramm-Leach-Bliley Act (GLBA)

GLBA requires financial institutions to explain their information-sharing practices to customers and to safeguard sensitive data. This includes the Financial Privacy Rule, Safeguards Rule, and Pretexting Protection, all of which directly impact how Fintechs handle and protect customer financial information.

3. State-Specific Data Privacy Laws (e.g., CCPA/CPRA, NYDFS Cybersecurity Regulation)

Beyond federal regulations, various state laws impose strict requirements on data privacy and cybersecurity. California’s CCPA/CPRA, for instance, grants consumers significant rights over their personal data, while New York’s Department of Financial Services (NYDFS) Cybersecurity Regulation (23 NYCRR 500) mandates comprehensive cybersecurity programs for financial institutions operating in New York. Fintechs must understand and comply with all applicable state laws relevant to their operations and customer base.

4. NIST Cybersecurity Framework

While not a regulation, the National Institute of Standards and Technology (NIST) Cybersecurity Framework provides a voluntary set of guidelines and best practices to help organizations manage and reduce cybersecurity risk. Many US regulatory bodies refer to NIST standards, making it a de facto standard for robust cybersecurity programs.

5. Emerging Regulations and AI Governance

As AI and machine learning become more integrated into Fintech operations, new regulations governing AI ethics, bias, and data usage are anticipated. Fintechs should proactively monitor these developments and build their AI systems with transparency, fairness, and security in mind.

Advanced Technologies for Enhanced Fintech Payment Security

Leveraging cutting-edge technologies is crucial for staying ahead of cybercriminals and fortifying Fintech Payment Security:

1. Artificial Intelligence (AI) and Machine Learning (ML) for Fraud Detection

AI and ML algorithms can analyze vast datasets in real-time to identify anomalies and patterns indicative of fraudulent activities more effectively than traditional rule-based systems. This includes:

- Behavioral Biometrics: Analyzing user behavior (e.g., typing patterns, mouse movements) to detect unusual activity.

- Predictive Analytics: Forecasting potential fraud based on historical data and current transaction characteristics.

- Adaptive Learning: Systems that continuously learn and improve their fraud detection capabilities over time.

2. Blockchain and Distributed Ledger Technology (DLT)

While often associated with cryptocurrencies, blockchain’s immutable and distributed nature offers significant security advantages for payment systems:

- Enhanced Transaction Security: Transactions recorded on a blockchain are highly resistant to tampering.

- Transparency and Auditability: DLT provides a transparent and auditable trail of transactions, making it harder for fraud to go unnoticed.

- Reduced Settlement Risk: Potential for faster and more secure settlement processes.

3. Zero Trust Architecture (ZTA)

Moving away from the traditional perimeter-based security model, Zero Trust operates on the principle of ‘never trust, always verify.’ Every user, device, and application attempting to access resources, whether inside or outside the network, must be authenticated and authorized. This significantly enhances Fintech Payment Security by:

- Micro-segmentation: Isolating network segments to limit lateral movement of attackers.

- Continuous Verification: Regularly re-authenticating and re-authorizing access based on context.

- Least Privilege Access: Ensuring users and systems only have the minimum necessary access rights.

4. Cloud Security Posture Management (CSPM) and Cloud Workload Protection Platforms (CWPP)

Many Fintechs operate in cloud environments. Ensuring the security of these environments is paramount:

- CSPM: Continuously monitors cloud configurations for misconfigurations, compliance violations, and security risks.

- CWPP: Protects workloads (VMs, containers, serverless functions) running in the cloud from various threats.

5. Quantum-Resistant Cryptography

As quantum computing advances, current encryption standards may become vulnerable. Fintechs should begin exploring and planning for the transition to quantum-resistant (post-quantum) cryptography to future-proof their data protection strategies.

Operational Best Practices for Sustained Security

Technology alone is not enough. Robust operational practices are vital for maintaining high levels of Fintech Payment Security:

1. Continuous Monitoring and Threat Intelligence

A proactive security posture requires constant vigilance:

- Security Information and Event Management (SIEM) / Security Orchestration, Automation, and Response (SOAR): Implement robust SIEM/SOAR solutions to aggregate, analyze, and respond to security alerts in real-time.

- Endpoint Detection and Response (EDR) / Extended Detection and Response (XDR): Gain comprehensive visibility and response capabilities across endpoints, networks, and cloud environments.

- Threat Intelligence Feeds: Subscribe to and integrate threat intelligence feeds to stay informed about emerging threats and vulnerabilities relevant to the Fintech sector.

2. Employee Training and Awareness

The human element is often the weakest link. Regular and comprehensive security training for all employees is critical:

- Phishing Simulations: Conduct regular simulated phishing attacks to test employee vigilance and educate them on identifying malicious emails.

- Security Awareness Programs: Educate employees on common cyber threats, secure coding practices, data handling policies, and incident reporting procedures.

- Culture of Security: Foster a company culture where security is everyone’s responsibility, from the CEO to the newest intern.

3. Third-Party Risk Management (TPRM)

Fintechs often rely on a network of third-party vendors, partners, and service providers. Each of these introduces potential security risks. A robust TPRM program is essential:

- Vendor Due Diligence: Thoroughly vet all third-party providers for their security posture and compliance.

- Contractual Obligations: Include clear security and compliance requirements in all vendor contracts.

- Continuous Monitoring: Regularly assess and monitor the security performance of third-party vendors.

- Supply Chain Security: Extend security scrutiny to the entire supply chain, understanding the risks introduced by upstream providers.

4. Regular Audits and Compliance Checks

Periodic internal and external audits ensure that security controls are effective and compliance requirements are met. This includes:

- PCI DSS Audits: Annual assessments for compliance.

- SOC 2 Audits: Demonstrating robust controls over security, availability, processing integrity, confidentiality, and privacy.

- Internal Security Audits: Regular reviews of security policies, procedures, and configurations.

5. Business Continuity and Disaster Recovery Planning

Even with the best security measures, incidents can occur. Having a well-defined business continuity and disaster recovery plan is crucial for minimizing downtime and ensuring rapid recovery:

- Data Backup and Restoration: Regular, secure backups of all critical data with tested restoration procedures.

- Redundancy: Implement redundant systems and infrastructure to ensure high availability.

- Incident Response Drills: Regularly conduct drills to test the effectiveness of incident response and disaster recovery plans.

The Future of Fintech Payment Security: Key Trends for 2026 and Beyond

Looking ahead, several trends will continue to shape the landscape of Fintech Payment Security:

- Increased Focus on API Security: With the rise of open banking and API-driven services, API security will become an even more critical area of focus, requiring dedicated tools and practices.

- Hyper-personalization of Security: Security measures will become more adaptive and personalized to individual user behavior and risk profiles, leveraging advanced AI.

- Decentralized Identity: Blockchain-based decentralized identity solutions could offer more secure and user-centric ways to manage digital identities, reducing reliance on centralized identity providers.

- Embedded Security: Security will be increasingly embedded directly into payment products and services, rather than being an add-on.

- Greater Collaboration: Increased collaboration between Fintechs, traditional financial institutions, regulators, and cybersecurity firms will be essential for sharing threat intelligence and developing collective defense strategies.

- ESG Considerations in Security: Environmental, Social, and Governance (ESG) factors will increasingly influence security strategies, with a focus on ethical AI, data privacy, and responsible technology use.

Conclusion: A Proactive Stance for Unwavering Trust

The digital payment landscape in 2026 will be characterized by both immense innovation and persistent threats. For US Fintechs, securing their digital payment infrastructures is not merely a technical challenge; it is a strategic imperative that underpins customer trust, regulatory compliance, and market competitiveness. By adopting a comprehensive approach that encompasses foundational security pillars, adheres to evolving regulatory mandates, leverages advanced technologies, and embeds robust operational practices, Fintechs can build resilient systems capable of withstanding the threats of tomorrow.

The journey towards impregnable Fintech Payment Security is continuous, demanding constant adaptation, investment, and a proactive mindset. Those Fintechs that prioritize security as a core business function will not only protect their assets and customers but also solidify their position as trusted leaders in the dynamic world of digital finance.