SASE in Fintech 2026: Securing Distributed US Workforces

The financial technology (fintech) sector in the United States is rapidly evolving, driven by innovation, digital transformation, and an increasingly distributed workforce. As 2026 approaches, the imperative for robust, agile, and scalable security solutions has never been greater. Traditional perimeter-based security models are proving inadequate against sophisticated cyber threats targeting sensitive financial data and distributed access points. This is where SASE Fintech Security emerges not just as a trend, but as a fundamental requirement for operational resilience and competitive advantage.

Adopting SASE in 2026: Streamlining Security for Distributed US Fintech Workforces

The shift to remote and hybrid work models, accelerated by recent global events, has fundamentally reshaped how US fintech companies operate. Employees access critical applications and sensitive data from various locations, using diverse devices, often outside the traditional corporate network. This paradigm shift has blurred the network perimeter, creating new vulnerabilities that conventional security architectures struggle to address effectively. The answer lies in a converged approach: Secure Access Service Edge (SASE).

By 2026, the adoption of SASE will be a non-negotiable for US fintechs aiming to maintain stringent security postures, ensure regulatory compliance, and support a dynamic, distributed workforce. This comprehensive guide delves into why SASE Fintech Security is crucial, its core components, the benefits it offers, implementation strategies, and what US fintechs need to consider for a successful transition.

The Evolving Threat Landscape for US Fintechs

Fintech companies are prime targets for cybercriminals due to the valuable financial data they handle. The threats are multifaceted and constantly evolving:

- Phishing and Social Engineering: Increasingly sophisticated attacks designed to trick employees into revealing credentials or installing malware.

- Ransomware: A persistent and growing threat that can cripple operations and lead to significant financial losses and reputational damage.

- Data Breaches: Unauthorized access to customer financial information, leading to regulatory fines, loss of trust, and legal repercussions.

- Insider Threats: Malicious or accidental actions by employees or former employees that compromise data security.

- API Vulnerabilities: As fintechs rely heavily on APIs for integration, vulnerabilities in these interfaces can expose sensitive data.

- Supply Chain Attacks: Compromising third-party vendors to gain access to the fintech’s network.

The distributed nature of modern fintech operations exacerbates these challenges. Devices outside the corporate firewall are harder to secure, and the sheer volume of remote access points creates a larger attack surface. This makes a centralized, cloud-native security model like SASE not just beneficial, but essential for robust SASE Fintech Security.

What is SASE and Why is it Critical for Fintech?

SASE (pronounced ‘sassy’) is a cybersecurity framework that converges wide area networking (WAN) and network security functions into a single, cloud-native service. Coined by Gartner in 2019, SASE combines networking capabilities (like SD-WAN) with comprehensive security functions (like Firewall as a Service, Secure Web Gateway, Cloud Access Security Broker, and Zero Trust Network Access) into a unified, globally distributed platform.

For US fintechs, SASE offers a transformative approach to security by:

- Securing the Distributed Workforce: It provides consistent security policies and enforcement regardless of user location or device, ideal for remote and hybrid teams.

- Enhancing Performance: By routing traffic through nearby SASE points of presence (PoPs), it minimizes latency and improves application performance, crucial for real-time financial transactions.

- Simplifying Management: Consolidating multiple security tools into a single platform reduces complexity, operational overhead, and the risk of misconfigurations.

- Enabling Zero Trust: SASE inherently supports a Zero Trust Network Access (ZTNA) model, where no user or device is trusted by default, requiring continuous verification. This is paramount for protecting sensitive financial data.

- Ensuring Regulatory Compliance: Fintechs operate under stringent regulations (e.g., GLBA, PCI DSS, SOX). SASE provides granular control, logging, and auditing capabilities necessary for demonstrating compliance.

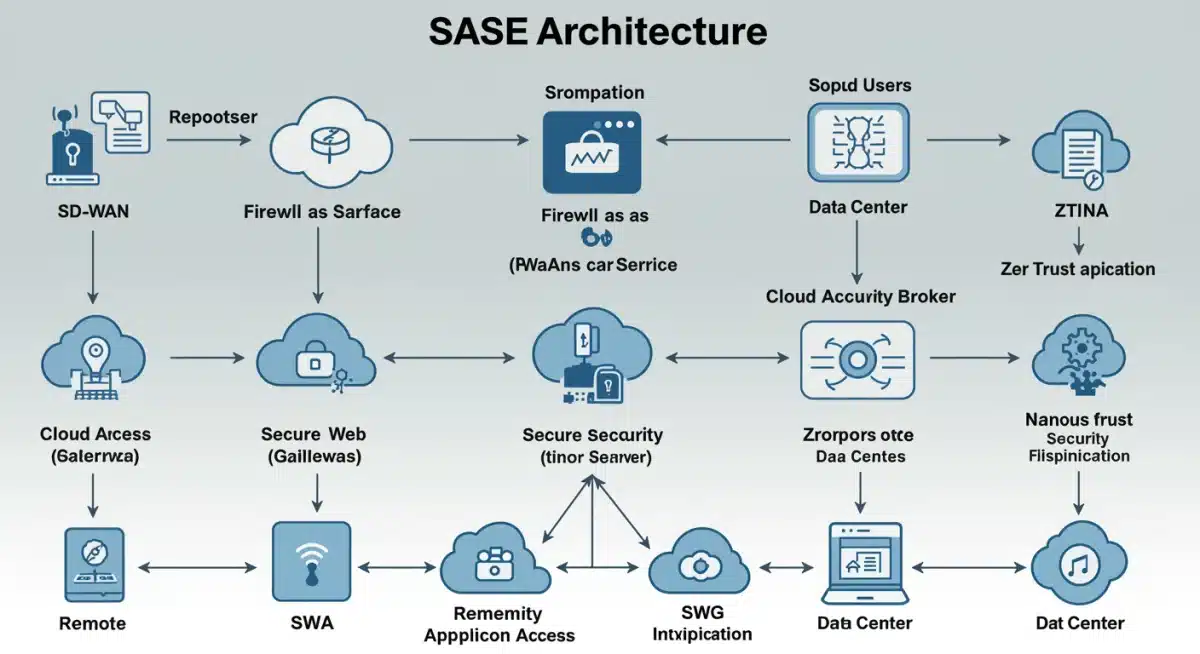

Key Components of a SASE Architecture for Fintech

A robust SASE implementation for fintech relies on the integration of several core technologies:

1. Software-Defined Wide Area Network (SD-WAN)

SD-WAN optimizes network traffic over various connection types, prioritizing critical financial applications and ensuring reliable, high-performance access for distributed users. It intelligently routes traffic to the nearest SASE PoP, reducing latency and improving the user experience, which is vital for time-sensitive financial operations.

2. Firewall as a Service (FWaaS)

FWaaS delivers firewall capabilities from the cloud, providing consistent policy enforcement for all users, regardless of their location. This eliminates the need for physical firewalls at each branch office or remote location, simplifying management and ensuring uniform protection across the entire fintech ecosystem. It’s a critical component for maintaining SASE Fintech Security.

3. Secure Web Gateway (SWG)

SWG protects users from web-based threats by filtering malicious content, enforcing acceptable use policies, and preventing access to unauthorized websites. For fintechs, this means protecting against phishing sites, malware downloads, and ensuring employees don’t access risky web content that could compromise sensitive data.

4. Cloud Access Security Broker (CASB)

CASB provides visibility and control over cloud application usage. It helps fintechs identify shadow IT, enforce data loss prevention (DLP) policies for cloud services, and ensure compliance with regulatory requirements when using SaaS applications like Salesforce, Microsoft 365, or specialized financial platforms. This is particularly important given the increasing reliance on cloud services within fintech.

5. Zero Trust Network Access (ZTNA)

ZTNA replaces traditional VPNs by providing secure, granular access to specific applications rather than the entire network. Access is granted based on user identity, device posture, and context, and is continuously verified. This ‘never trust, always verify’ approach is foundational for protecting highly sensitive financial data and intellectual property in a distributed environment, forming the bedrock of effective SASE Fintech Security.

6. Data Loss Prevention (DLP)

Integrated DLP capabilities within SASE help fintechs prevent sensitive financial data from leaving the organization’s control, whether through email, cloud applications, or endpoint devices. This is crucial for protecting customer financial information, proprietary algorithms, and other confidential data.

Benefits of SASE for US Fintechs by 2026

The adoption of SASE offers a multitude of benefits that directly address the unique security and operational challenges faced by US fintechs:

Enhanced Security Posture

- Comprehensive Threat Protection: SASE integrates multiple security functions, providing a layered defense against a wide range of cyber threats, from malware and phishing to sophisticated zero-day attacks.

- Consistent Policy Enforcement: Security policies are applied uniformly across all users, devices, and locations, eliminating security gaps that arise from disparate on-premise and cloud solutions.

- Reduced Attack Surface: ZTNA minimizes exposure by granting least-privilege access to specific applications, rather than broad network access.

- Real-time Threat Intelligence: Cloud-native SASE platforms leverage global threat intelligence, providing up-to-the-minute protection against emerging threats.

Improved Operational Efficiency and Agility

- Simplified Management: Consolidating security and networking into a single platform reduces the complexity of managing multiple point solutions, freeing up IT resources.

- Scalability: SASE easily scales to accommodate growth in users, devices, and applications without significant infrastructure investments, ideal for rapidly expanding fintechs.

- Faster Deployment: Cloud-native deployment means new security policies and services can be rolled out quickly across the entire organization.

- Optimized Network Performance: SD-WAN capabilities ensure low-latency access to cloud applications and financial services, improving productivity for distributed teams.

Cost Savings

- Reduced Hardware Costs: Eliminates the need for expensive on-premise security appliances and their associated maintenance.

- Lower Operational Expenses: Streamlined management and automation reduce the operational burden on IT security teams.

- Consolidated Vendor Management: Dealing with fewer vendors for security and networking simplifies procurement and support.

Regulatory Compliance and Governance

US fintechs operate under a strict regulatory framework, including the Gramm-Leach-Bliley Act (GLBA), Payment Card Industry Data Security Standard (PCI DSS), Sarbanes-Oxley Act (SOX), and state-specific data privacy laws. SASE significantly aids in achieving and maintaining compliance:

- Granular Access Control: ZTNA ensures only authorized personnel can access sensitive financial data and applications, a key requirement for many regulations.

- Data Loss Prevention (DLP): Prevents unauthorized exfiltration of sensitive customer data, directly addressing data protection mandates.

- Auditing and Logging: SASE platforms provide comprehensive logs of network traffic and user activities, essential for demonstrating compliance during audits.

- Consistent Policy Enforcement: Ensures that security controls are uniformly applied across all environments, reducing the risk of non-compliance due to inconsistent configurations.

Implementing SASE in US Fintechs: A Strategic Roadmap for 2026

Transitioning to SASE requires a strategic approach. Here’s a roadmap for US fintechs to consider:

1. Assess Current Infrastructure and Needs

- Inventory Assets: Understand all applications (cloud, on-premise), data locations, user types, and devices.

- Identify Gaps: Pinpoint current security vulnerabilities and inefficiencies in your existing network and security architecture.

- Define Business Requirements: What are the specific performance, security, and compliance needs of your fintech operations? Consider future growth and evolving regulatory landscapes.

2. Phased Rollout and Pilot Programs

- Start Small: Begin with a pilot program involving a small group of users or a specific branch office to test the SASE solution’s effectiveness and address any initial challenges.

- Iterative Deployment: Gradually expand the SASE deployment across the organization, learning from each phase and refining the implementation.

3. Vendor Selection

- Integrated vs. Best-of-Breed: Decide whether to opt for a single vendor offering a comprehensive SASE platform or integrate components from multiple specialized vendors. For fintechs, an integrated platform often simplifies management and ensures tighter security correlation.

- Regional PoPs: Ensure the chosen SASE vendor has a strong presence with PoPs across the US to guarantee low-latency access for all distributed workforces.

- Fintech-Specific Features: Look for vendors with experience in financial services, offering features like advanced threat protection for financial transactions, robust data encryption, and strong compliance reporting.

4. Training and Change Management

- Employee Education: Train employees on new access procedures, security policies, and how to use SASE-protected applications.

- IT Staff Training: Ensure your IT and security teams are thoroughly trained on managing and optimizing the SASE platform.

- Communication: Clearly communicate the benefits of SASE to all stakeholders, emphasizing improved security and user experience.

5. Continuous Monitoring and Optimization

- Performance Monitoring: Regularly monitor network performance, application access, and security events.

- Policy Review: Continuously review and update security policies to adapt to evolving threats and business needs.

- Compliance Audits: Conduct regular internal and external audits to ensure ongoing regulatory compliance.

Challenges and Considerations for SASE Adoption in Fintech

While the benefits of SASE are clear, fintechs must also navigate potential challenges:

- Legacy Systems Integration: Integrating SASE with existing legacy financial systems and applications can be complex. A phased approach and careful planning are essential.

- Data Residency and Sovereignty: Ensuring that sensitive financial data remains within specific geographic boundaries, especially important for US-based fintechs, requires careful consideration of cloud provider locations and compliance with local regulations.

- Vendor Lock-in: Opting for a single, comprehensive SASE vendor might lead to vendor lock-in. Evaluate vendor flexibility and interoperability carefully.

- Skill Gap: Managing a converged SASE platform requires a new set of skills from IT and security teams. Investment in training or hiring new talent may be necessary.

- Initial Investment: While SASE offers long-term cost savings, the initial investment in a new platform and migration can be substantial.

The Future of SASE Fintech Security in 2026 and Beyond

By 2026, SASE will no longer be an option but a foundational element of cybersecurity strategy for leading US fintech organizations. The convergence of networking and security at the cloud edge is perfectly suited to the demands of digital finance, remote work, and stringent regulatory environments. As fintech continues to innovate, adopting cutting-edge technologies like AI, blockchain, and real-time payment systems, the underlying security infrastructure must be equally advanced and adaptable. SASE provides this agility.

Looking ahead, we can expect SASE platforms to become even more intelligent, incorporating advanced AI and machine learning for predictive threat detection, automated policy enforcement, and self-healing network capabilities. The integration with other emerging security technologies, such as Extended Detection and Response (XDR) and Security Orchestration, Automation, and Response (SOAR), will further enhance the defensive capabilities of SASE Fintech Security.

Furthermore, the concept of ‘Security Service Edge’ (SSE), which focuses purely on the security aspects of SASE, may see increased adoption as some organizations opt to decouple networking and security for specific use cases. However, for most fintechs seeking holistic protection and performance optimization for their distributed workforces, the full SASE model will remain the preferred choice.

Conclusion

The journey towards robust, future-proof security for US fintechs culminates in the strategic adoption of SASE. By 2026, the competitive landscape will demand not just innovative financial products, but also an unwavering commitment to data security and operational resilience. SASE offers the architectural framework to achieve this, providing a unified, cloud-native solution that protects distributed workforces, safeguards sensitive financial data, ensures regulatory compliance, and drives operational efficiency.

Fintech leaders who embrace SASE Fintech Security now will be well-positioned to navigate the complexities of the digital future, mitigate evolving cyber threats, and confidently expand their services to meet the demands of a dynamic global economy. The time to act is now, to build a secure and agile foundation for the fintech innovations of tomorrow.

The move to SASE is not merely a technological upgrade; it’s a strategic imperative for any US fintech aiming for sustainable growth and unwavering trust in an increasingly interconnected and threat-laden world. Prepare your organization for 2026 by prioritizing a comprehensive SASE strategy today.